GPT Healthcare IPO: Is It A Healthy Investment Opportunity?

Get a detailed overview of GPT Healthcare Ltd IPO, including GMP, verdict, issue details, and the company's strengths and risks.

The initial public offer (IPO) of GPT Healthcare Ltd, which kicked off today, will close for subscription on Monday, February 26. The healthcare firm is looking to raise Rs 525.14 crore through its IPO, which comprises an Offer for Sale (OFS) of up to Rs 485.14 crore by the selling shareholders. The firm has announced a price band of Rs 177 to Rs 186 per share for its IPO. Prospective investors can bid in lots, with each lot consisting of 80 shares. To apply for the IPO, the minimum investment is set at Rs 14,880 (calculated as 80 x 186).

According to market observers, shares of GPT Healthcare Ltd have not yet started trading in the grey market. The public offer is anticipated to debut on BSE and NSE on the 29th of February, 2024.

GPT Healthcare Anchor Round

Prior to issue opening, on February 21, GPT Healthcare Ltd successfully secured Rs 157.54 crore from anchor investors, by allocating 84,69,996 equity shares at Rs 186/ share. Some notable Foreign and Domestic Institutions that participated in the anchor round include Kotak Mutual Fund, Axis Mutual Fund, Bandhan Mutual Fund, Aditya Birla Life Insurance, Societe Generale, Duro One Investments Ltd, India Capital Growth Fund, Copthall Mauritius, and LC Pharos Multi Strategy Fund, among others.

About GPT Healthcare Ltd

GPT Healthcare runs a network of mid-sized hospitals that offer full-service healthcare solutions, specializing in both secondary and tertiary care. It delivers an extensive array of medical services covering more than 35 specialties and super-specialties.

As of September 30, 2023, the firm managed 4 multispecialty hospitals located in West Bengal and Tripura, providing a total of 561 beds. It is now looking to extend its network of hospitals to Eastern India.

Strengths

- Diverse and Strong Operational Footprint: GPT Healthcare benefits from a diversified operational base across multiple specialties, with a large part of its revenue coming from private insurance and walk-in cash patients, reflecting a high demand for its services.

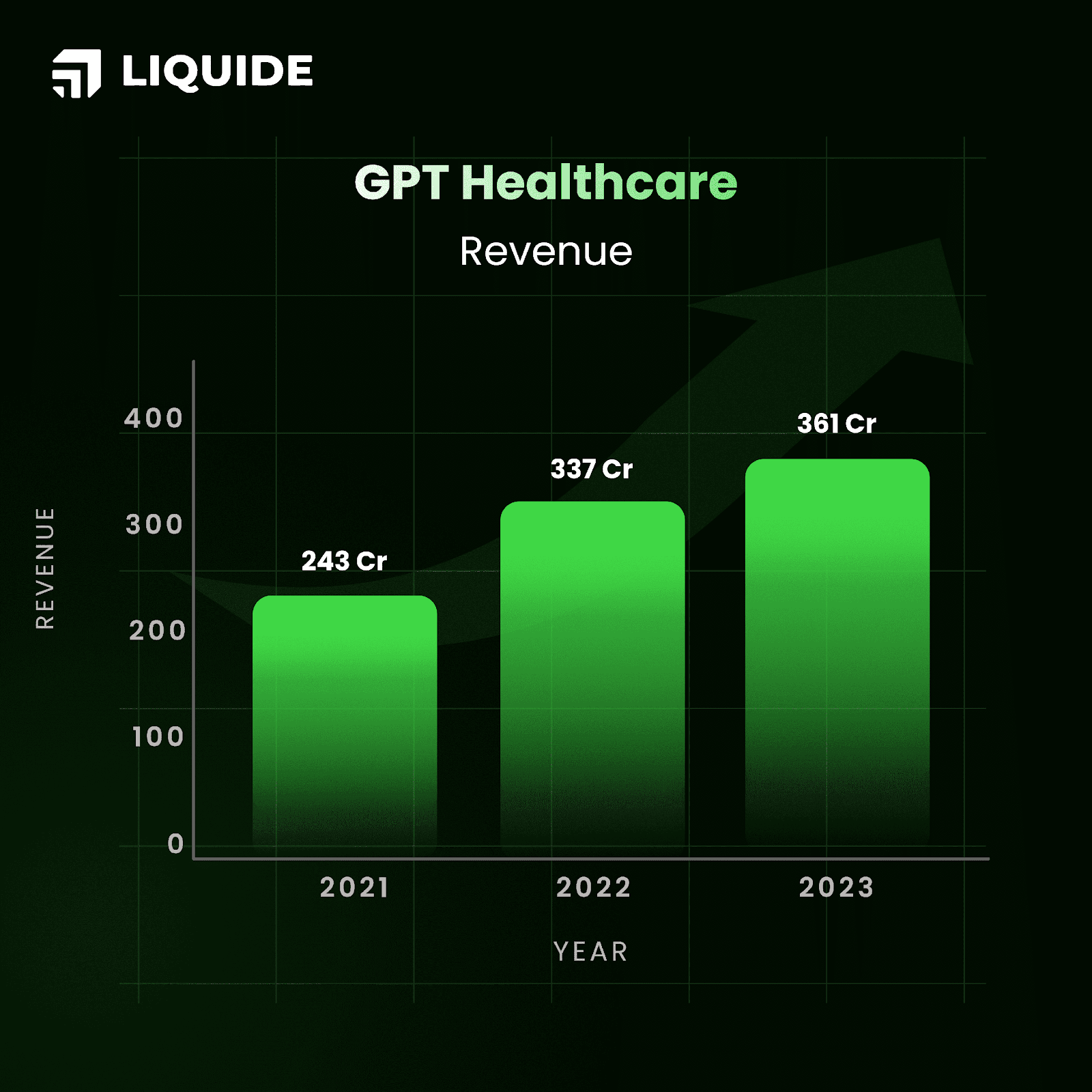

- Impressive Financial Growth: The firm has demonstrated outstanding financial performance, with a Compound Annual Growth Rate (CAGR) of 22% in Revenue from Operations between FY21 and FY23, alongside a commendable 21% growth in EBITDA.

- Robust Return Ratios: The firm enjoys healthy return ratios, with a Return on Equity (ROE) of 23.59% and a Return on Capital Employed (ROCE) of 26.09%.

- Improved Bed Occupancy Rates: There has been a significant improvement in bed occupancy rates at GPT Healthcare, increasing from 48% in FY21 to 58.92% in FY23, and further to 59.92% by September 2023.

Key Concerns

- Revenue Concentration Risk: A substantial portion, nearly 70%, of GPT Healthcare's revenue is sourced from three hospitals in West Bengal. Fluctuations in West Bengal's economic or political landscape could significantly impact the company's operations.

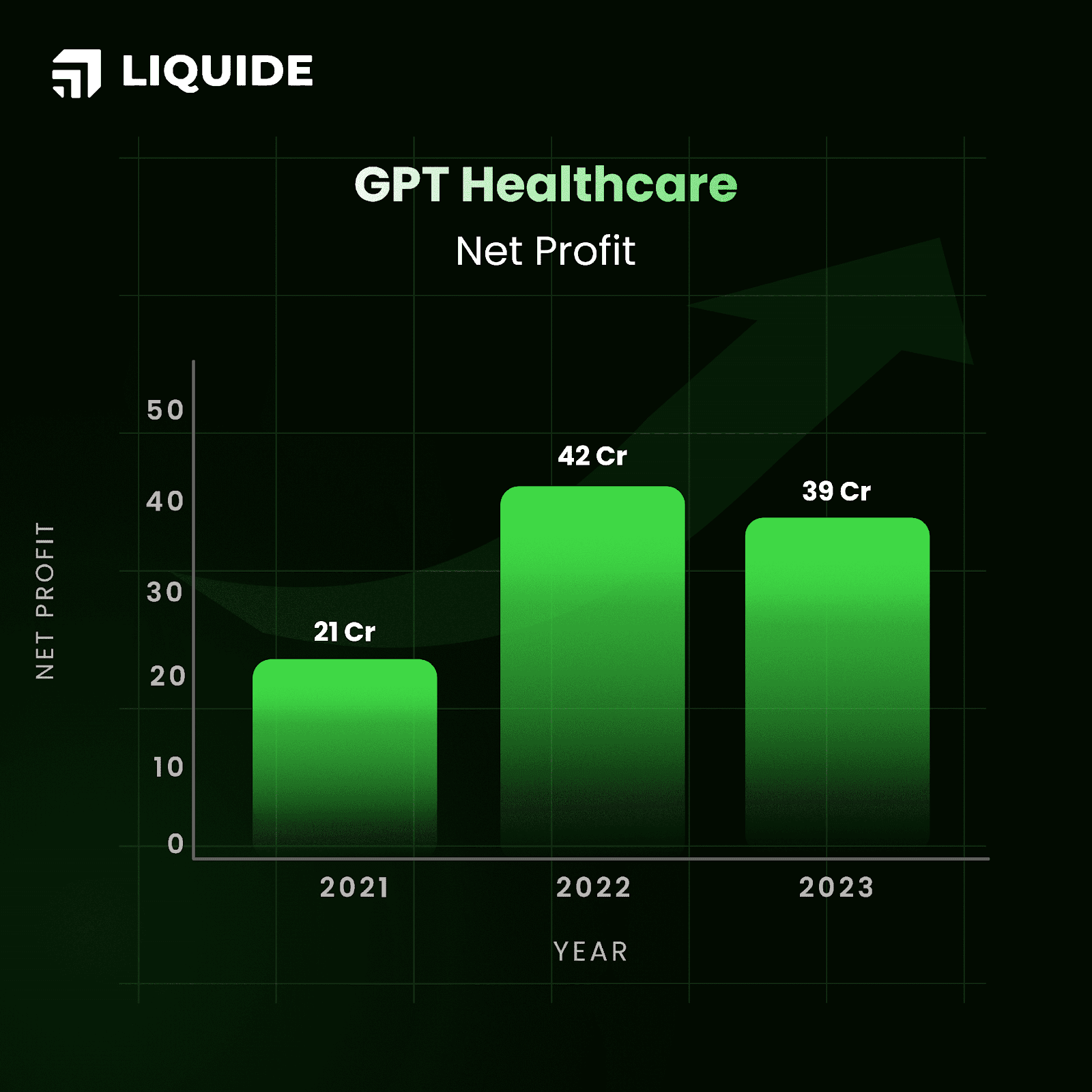

- Inconsistency in Earnings: The Net Profit rose from Rs 21.09 crore in FY21 to Rs 41.66 crore in FY22, before decreasing to Rs 39 crore in FY23. In a similar trend, the net profit margin grew from 8.48% in FY21 to 12.17% in FY22, then dropped to 10.64% in FY23.

- Concerns Related to the Promoter Group: Ishwari Prasad Tantia, a key figure in the Promoter Group, has been identified as a Wilful Defaulter by some financial entities. Furthermore, the company has previously encountered issues with regulatory compliance. Any negative rulings or fines from banks, the Reserve Bank of India (RBI), or the Securities and Exchange Board of India (SEBI) against any promoter or the company itself could affect its business operations.

- Comparative Lower Bed Occupancy Rates: GPT Healthcare’s bed occupancy rates fall short when compared to those of its peers in the market. Inability to sustain or improve these rates could hinder the company from realizing expected returns.

Conclusion

GPT Healthcare operates in markets that are both densely populated and under-served, particularly in Eastern India where there is a notable scarcity of healthcare professionals. With only five doctors and 12.7 nurses per 10,000 people, this region has the lowest density of healthcare workers in the country. This positions GPT Healthcare advantageously to cater to the high demand for healthcare services in the area.

In terms of valuation, the IPO seems fairly priced at a Price-to-Earnings (P/E) ratio of 38x, which is below the industry average, suggesting potential for a positive re-rating in the future. Nonetheless, GPT Healthcare is yet to successfully expand its footprint outside its home territory and needs to improve its bed occupancy rates further for better financial performance.

Considering these factors, investors looking for immediate gains from the IPO might choose to stay away, while long-term investors might prefer to observe the company's performance and reassess based on the improvement in financial metrics over time.

Unlock a world of financial opportunities with Liquide, the ultimate app for the modern investor. Featuring advanced tools like LiMo, India's pioneering AI co-pilot for stock investing, Liquide empowers you with insights that can guide your financial journey. Stay updated with thorough market analysis, expert recommendations, and real-time information. Download the Liquide App today from the Google Play Store or Apple Appstore and embark on a journey of informed and successful investing. Don't miss out on the powerful features that can shape your financial future.