Waterways Leisure Tourism IPO Review: Subscription Status, GMP & Analysis

Waterways Leisure Tourism IPO 2026 opens with muted subscription and subdued GMP. Read our detailed analysis of its price band, issue size, business model, financials, strengths, risks and investor outlook.

The initial public offering (IPO) of Waterways Leisure Tourism Ltd (WLTL) opened to muted investor response on Tuesday, June 23, 2026.

As of 11:30 AM on Day 1 of bidding, the issue was subscribed 0.07 times overall. The retail portion saw 0.35 times subscription, while the non-institutional investor (NII) category received 0.01 times bids. The qualified institutional buyer (QIB) segment was yet to see participation.

Meanwhile, the grey market premium (GMP) remained subdued in the unlisted market, indicating expectations of a potentially muted listing.

Before making an investment decision, explore our comprehensive, data-driven IPO analysis to understand how the company’s numbers stack up. Our detailed report covers WLTL's growth prospects, financial performance, key strengths and potential red flags.

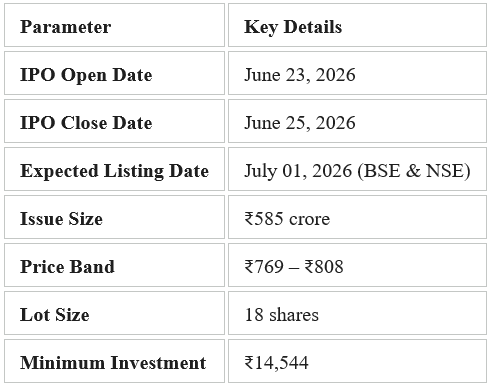

Waterways Leisure Tourism IPO Details, Date & Price Band

Waterways Leisure Tourism: Business Overview

WLTL operates Cordelia Cruises, India’s leading domestic ocean cruise brand, focused on delivering premium leisure travel experiences.

The firm currently operates the ‘MV Empress’, a 2,005-passenger cruise ship with 796 cabins, covering key Indian destinations such as Mumbai, Goa, Kochi, Chennai, Lakshadweep, Visakhapatnam and Puducherry. It also offers select international itineraries to Sri Lanka, Thailand, Singapore and Malaysia.

The company’s revenue is primarily driven by cruise ticket sales, which accounted for 91% of FY26 revenue. The remaining revenue is generated through onboard spending, including specialty dining, entertainment, shore excursions, Wi-Fi, spa services and other premium offerings.

Waterways Leisure Tourism: Key Strengths

- Market Leadership: WLTL commands a strong leadership position in India’s overnight ocean and coastal cruise industry, with an ~79% market share by value as of FY25. This makes it one of the most dominant players in a niche but rapidly growing tourism segment.

- Strong Direct Booking Mix: In FY26, WLTL directly sold ~62% of its total cabins. This direct-to-consumer squeeze keeps customer acquisition costs low by reducing commissions paid to travel agents and thus supports better margins.

- Healthy Occupancy Rate: WLTL maintains a healthy occupancy rate of ~85%, supported by an average ticket price of around ₹11,000 per passenger. Going forward, it plans to significantly expand capacity through the addition of two larger cruise vessels, Norwegian Sky and Norwegian Sun, which could nearly triple its passenger-carrying capacity.

Waterways Leisure Tourism: Risk Factors

- Limited Operating History: WLTL was incorporated in November 2020 and its cruise operations began only in September 2021. Its limited operating history at this scale makes it difficult to assess long-term business performance, growth prospects and potential risks.

- Earnings Volatility: WLTL has incurred losses in the past and may continue to face profitability pressure in the future. While the firm reported a profit of ₹168 crore in FY25, this was mainly due to the recognition of exceptional items.

- Cash Flow Concerns: WLTL reported negative operating cash flows in FY26. If such cash flow pressure continues, it may impact liquidity, day-to-day operations and overall financial flexibility.

- High Dependence on One Vessel: WLTL currently depends on a single cruise vessel, increasing operational risk in case of downtime, repairs or disruptions. Additionally, ~91% of revenue comes from cruise ticket sales, making the business highly dependent on passenger demand and occupancy levels.

Final Thoughts: Should You Subscribe to Waterways Leisure Tourism’s IPO?

WLTL, which operates Cordelia Cruises, holds a dominant position in India’s growing cruise tourism market and has maintained healthy occupancy levels.

However, despite turning profitable, EBITDA margins have declined. At nearly 101x P/E, the IPO appears aggressively valued, offering limited margin of safety even though the sector has favourable long-term growth potential.

The business also carries high concentration risk. WLTL currently depends entirely on a single vessel, MV Empress and ~67% of FY26 passengers boarded from Mumbai. Any port disruption, adverse weather event or operational issue could materially impact the entire business.

Moreover, the company has a volatile earnings history and a relatively limited operating track record, making future growth visibility uncertain at this stage.

Given these considerations, investors may be better placed waiting for at least the next two quarters of financial performance before considering any exposure.

For a deep dive into other IPOs, explore: IPO Corner on Liquide

Disclaimer: Investment in securities market are subject to market risks. Read all the related documents carefully before investing.

The content provided in this blog is purely for informational and educational purposes only and does not constitute explicit investment advice, buy/ sell/ subscribe recommendations or a solicitation to trade.

The analysis of Waterways Leisure Tourism Ltd is based on publicly available data, the Red Herring Prospectus (RHP) and market trends. Grey Market Premium (GMP) data is highly volatile, speculative, unregulated and should not be used as the primary basis for investment decisions.

Investors are strongly advised to consult with a SEBI-registered financial advisor before executing any trading strategies or making investment decisions.

For a detailed disclaimer, please visit our official website https://liquide.life/