Waaree Energies Ltd IPO Analysis 2024: Should You Subscribe?

Get a detailed overview of Waaree Energies IPO, including GMP, Subscription Status, Financial Analysis, Risk Factors and Expert Verdict.

The IPO (initial public offering) of Waaree Energies Ltd (Waaree) commences on October 21 and concludes on October 23, 2024. The offering, carrying a massive Grey Market Premium (GMP) of 100.5%, attracted significant interest on its first day of bidding.

However, investors need a clear understanding of both potential rewards and risks before subscribing. This IPO analysis provides a comprehensive review to help make an informed decision.

Waaree Energies IPO Details

- Issue Size: Rs 4,321.44 crore

- Fresh Issue: Rs 3,600 crore

- OFS: Rs 721.44 crore

- Price Band: Rs 1,427 – Rs 1,503

- Lot Size: 9 shares

- Listing Date: October 28, 2024

Waaree Energies IPO Subscription Status

The IPO of Waaree Energies Ltd witnessed robust demand on its first day, with subscriptions reaching 3.41 times by 5 p.m. Non-institutional investors subscribed 8.09 times their allocation, while retail investors subscribed 3.29 times. Meanwhile, qualified institutional buyers subscribed just 0.08 times their reserved portion.

Overview of Waaree Energies

Waaree is India’s largest solar PV module manufacturer, with 13.3 GW capacity across Gujarat and Uttar Pradesh. It is now expanding internationally by setting up a 1.6 GW solar PV module facility in Texas (USA) to benefit from US Inflation Reduction Act incentives.

Waaree has also been awarded a solar PLI for a 6 GW integrated manufacturing facility, which will boost its total capacity to over 20 GW in 2-3 years. Domestically, it is building a 5.4 GW solar cell facility in Gujarat to strengthen supply chains and margins, set to be operational by year-end.

Waaree Energies Key Strengths

- Market Leadership: Waaree holds the distinction of being India's largest solar PV module manufacturer, with an unmatched installed capacity of 12 GW as of June 30, 2024. In FY24, it ranked second in operating income among all Indian solar PV module manufacturers.

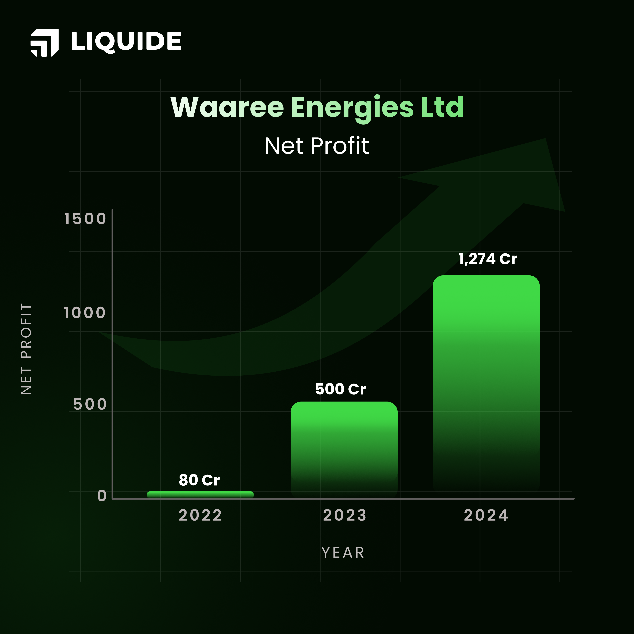

- Exceptional Financial Growth: Waaree has demonstrated significant growth, with its operational revenue and net profit achieving CAGRs of 100% and 300%, respectively, from FY22 to FY24.

- Solid Return Ratios: Waaree’s financial efficiency is highlighted by impressive return metrics, with a Return on Equity of 30.26% and a Return on Capital Employed of 26.29% in FY24.

- Increasing Profitability: Over recent years, Waaree has consistently improved its EBITDA and Net Profit margins, which stood at 15.56% and 10.96%, respectively, as of March 31, 2024.

- Robust Order Book: As of June 30, 2024, Waaree maintained a robust order book, with pending orders totaling 16.66 GW for solar PV modules and an additional 3.75 GW from its US subsidiary, Waaree Solar Americas Inc.

- Strong Industry Tailwinds: Following post-Covid disruptions, India’s solar module manufacturing has surged due to government initiatives like the PLI scheme, Pradhan Mantri KUSUM and Suryodaya Yojana. Solar capacity has tripled in the last 6 years, reaching 87.2 GW by July.

Waaree Energies Risk Factors

- Client Concentration: Waaree’s revenue concentration is high, with its top 1, 5, and 10 customers representing 9%, 40%, and 57% of its operational revenue as of FY24, respectively. This dependency on a limited number of clients exposes the company to significant risk if there is a reduction or delay in orders.

- Geographical Concentration: With four out of five of Waaree's operational manufacturing facilities located in Gujarat, the company is susceptible to risks associated with local and regional factors that could hinder operations and negatively impact business performance and cash flows.

Waaree Energies Valuation & Recommendation

Waaree Energies Ltd has shown impressive revenue and EBITDA growth in recent years, with its turnover increasing nearly six-fold since FY21 to over Rs 11,000 crore, driven by favourable government policies. Scale and operational efficiencies have significantly boosted EBITDA and net profit margins.

In terms of valuations, the IPO seems reasonably priced with a price-to-earnings (P/E) ratio of 31x based on FY24 earnings.

Despite concerns about a domestic supply surplus and competitive pressures from Chinese manufacturers, Indian firms benefit from various levels of government protection. As the largest solar PV module producer in India, Waaree stands to gain significantly from the booming solar energy sector.

Given the fair valuations, impressive growth metrics, strategic expansion initiatives and strong industry tailwinds, investors may consider subscribing to this IPO from a medium-to-long term perspective.

For a deep dive into other IPOs, explore: IPO Corner on Liquide