Turtlemint Fintech Solutions IPO Review: Subscription Status, GMP & Analysis

Turtlemint IPO 2026 opens with muted subscription and subdued GMP. Read our detailed analysis of its price band, issue size, business model, financials, strengths, risks and investor outlook.

The initial public offering (IPO) of Turtlemint Fintech Solutions Ltd (Turtlemint) opened to muted investor response on Friday, June 19, 2026.

As of 12:10 PM on Day 1 of bidding, the issue was subscribed 0.03 times overall. The retail portion saw 0.16 times subscription, while the non-institutional investor (NII) category received 0.01 times bids. The qualified institutional buyer (QIB) segment was yet to see participation.

Meanwhile, the grey market premium (GMP) remained subdued in the unlisted market, indicating expectations of a potentially muted listing.

Before making an investment decision, explore our comprehensive, data-driven IPO analysis to understand how the company’s numbers stack up. Our detailed report covers Turtlemint’s growth prospects, financial performance, key strengths and potential red flags.

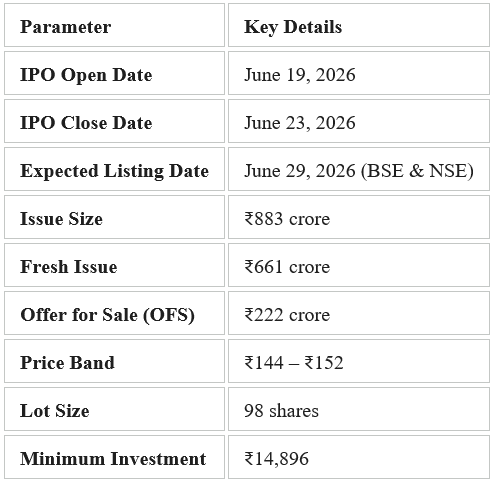

Turtlemint Fintech Solutions IPO Details, Date & Price Band

Turtlemint Fintech Solutions: Business Overview

- Turtlemint is a leading technology-enabled insurance distribution platform in India, connecting customers, insurance advisors and insurers through a scalable phygital ecosystem.

- The company pioneered the Point of Sale Person (PoSP) distribution model and has built one of the largest certified PoSP networks in the industry, with 631,885 Digital Partners as of December 2025.

- Its platform enables Digital Partners to sell and service insurance products across health, life and motor segments, while offering customers product comparison, advisory support, policy issuance, renewals and claims assistance.

Turtlemint Fintech Solutions: Key Strengths

- Strong Growth: The company has significantly outpaced the broader retail insurance market in terms of Gross Direct Premium Income (GDPI). While retail health, retail life new business and motor insurance grew at 10.3% CAGR between FY20 and FY25, Turtlemint’s GDPI growth in these categories was nearly 3x higher.

- Extensive Reach: Between April 2022 and December 2025, Turtlemint facilitated nearly 21.87 million insurance policies across 19,171 PIN codes, covering around 98% of India’s postal network.

- Deep B30+ Presence: Turtlemint has strong penetration in underserved B30+ markets, which exclude India’s top 30 cities by population. As of December 31, 2025, 80% of its Digital Partners and 75% of Platform Premium distributed came from B30+ markets.

Turtlemint Fintech Solutions: Risk Factors

- Weak Financials: Turtlemint reported net losses in 9M FY26, 9M FY25 and each of the last three financial years. It also recorded a significant decline in operating revenue, which fell by 81% from ₹4,199 million in FY23 to ₹786 million in FY24, primarily due to a reduction in income from marketing fees.

- Losses in Subsidiaries: Turtlemint’s subsidiaries, Turtlemint Insurance Broking Services Pvt Ltd (TIB) and Turtlemint Mutual Funds Distributors Pvt Ltd (TMF), have also incurred losses in the past. Continued losses at the subsidiary level could adversely impact the company’s overall financial position and operating performance.

- Erosion in Net Worth: Turtlemint’s net worth has been consistently eroding due to accumulated losses. Net worth declined significantly from ₹7,435 million in FY23 to ₹4,105 million in FY25 and further to ₹2,957 million in 9M FY26. Return on Net Worth (RoNW) also deteriorated sharply to negative 47.29% in FY25.

- Cash Flow Concerns: Turtlemint reported negative operating cash flows in 9M FY26, 9M FY25 and the last three fiscal years. Sustained negative cash flows may put pressure on liquidity, affect day-to-day operations and limit financial flexibility.

- High Employee Attrition: Employee retention remains a concern, with permanent employee attrition at 48.5% in FY24 and 38.54% in FY25. The resignation of the Chief Human Resources Officer in September 2024 further adds to leadership concerns and workforce stability.

- Partner Concentration: Despite its pan-India presence, Turtlemint faces significant concentration risk. In 9M FY26, ~72% of operating revenue was generated from its top 10 insurer partners.

- Geographic Concentration: ~30% of platform premium, excluding enterprise business, was concentrated in just two states: Maharashtra and Gujarat, exposing the company to regional and partner-related volatility.

Final Thoughts: Should You Subscribe to Turtlemint Fintech’s IPO?

Turtlemint remains a loss-making company with a negative RoNW of (47.29%), reflecting weak return metrics and continued pressure on shareholder value.

The company operates in a high-growth insurance distribution segment, supported by rapid expansion in the PoSP model and rising digital adoption in insurance.

Turtlemint has built one of the largest PoSP-led distribution networks in its peer group, supported by 45 insurer partnerships and a wide pan-India digital partner base. However, the model remains exposed to regulatory changes, insurer relationships and high partner payout costs.

Revenue history has been volatile, with FY24 operating revenue declining sharply by over 81% YoY, making future growth difficult to forecast with confidence.

Despite strong market reach and favourable industry tailwinds, continued losses, negative operating cash flows and eroding net worth make the IPO unattractive at this stage.

It would be prudent for investors to assess the company’s financial performance over the next two quarters before considering any exposure.

For a deep dive into other IPOs, explore: IPO Corner on Liquide

Disclaimer: Investment in securities market are subject to market risks. Read all the related documents carefully before investing.

The content provided in this blog is purely for informational and educational purposes only and does not constitute explicit investment advice, buy/ sell/ subscribe recommendations or a solicitation to trade.

The analysis of Turtlemint Fintech Solutions Ltd is based on publicly available data, the Red Herring Prospectus (RHP) and market trends. Grey Market Premium (GMP) data is highly volatile, speculative, unregulated and should not be used as the primary basis for investment decisions.

Investors are strongly advised to consult with a SEBI-registered financial advisor before executing any trading strategies or making investment decisions.

For a detailed disclaimer, please visit our official website https://liquide.life/