Manba Finance IPO Analysis 2024: Should You Subscribe?

Get a detailed overview of Manba Finance IPO, including GMP, Subscription Status, Financial Analysis, Risk Factors and Expert Verdict.

The IPO (initial public offering) of Manba Finance Ltd (MFL) commences on September 23 and concludes on September 25, 2024. The offering, carrying a Grey Market Premium (GMP) of 50%, attracted significant interest on its first day of bidding.

However, investors need a clear understanding of both potential rewards and risks before subscribing. This IPO analysis provides a comprehensive review to help make an informed decision.

Manba Finance IPO Details

- Issue Size: Rs 150.84 crore

- Price Band: Rs 114 – Rs 120

- Lot Size: 125 shares

- Listing Date: September 30, 2024

Manba Finance IPO Subscription Status

The IPO of Manba Finance Ltd witnessed robust demand on its first day, with subscriptions reaching 23.35 times by 5 p.m. Non-institutional investors subscribed 42.16 times their allocation, while retail investors subscribed 27.32 times. Meanwhile, qualified institutional buyers subscribed 2.29 times their reserved portion.

Overview of Manba Finance

MFL is a non-banking financial company (NBFC) that has been operational for over 30 years. It primarily provides two-wheeler loans to both salaried and self-employed individuals, with an average loan amount of Rs 80,000. The firm has expanded its portfolio to include loans for used cars, electric three-wheelers, small businesses, and personal loans. It now aims to penetrate new markets to expand its loan book on a sustainable basis across various credit cycles.

Manba Finance Key Strengths

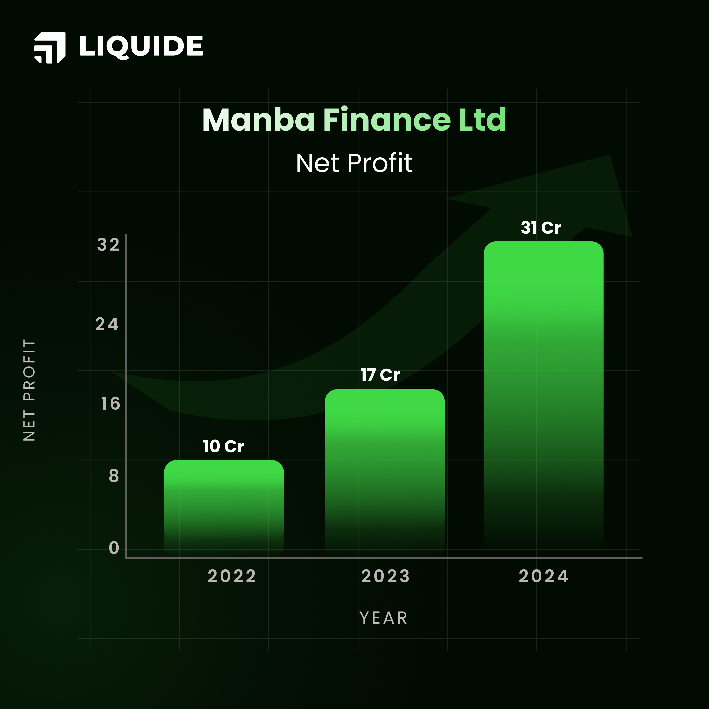

- Strong Financial Growth: MFL has exhibited a robust growth trajectory, with its interest income and net profit posting compounded annual growth rates (CAGRs) of 34% and 80%, respectively, from FY22 to FY24.

- Robust Growth in AUM: Over the past three years, MFL’s Assets Under Management (AUM) have grown at an impressive CAGR of 37%, reaching Rs 936.85 crore by FY24.

Manba Finance Risk Factors

- Rising NPAs: MFL's net NPAs have slightly increased to 3.16% in FY24 from 3.14% in FY23, and its gross NPAs of 4% are higher than those of its peers.

- Cash Flow Issues: Over the past two years, MFL has experienced negative cash flows from operating activities. Persistent negative cash flows could jeopardize its ability to fulfil cash requirements, potentially affecting its operational effectiveness and growth plans.

- Geographic Concentration: MFL’s operations are mainly concentrated in six states across western, central, and northern India, with Maharashtra alone contributing to 65% of its total AUM. Any adverse developments in these regions could negatively impact its operational and financial results.

- Limited Scale of Operations: MFL operates on a small scale with a moderately seasoned and concentrated product range; new vehicle loans constitute 98% of the total loan book, targeting primarily small and economically vulnerable borrowers.

- Intense Market Competition: MFL faces increasing competition in the low-ticket financing sector, not only from large, established players with nationwide coverage such as Mahindra Finance and Shriram Finance but also from small finance banks and lending platforms.

- Legal Concerns: MFL is involved in certain legal disputes, involving its promoters and directors. Any unfavourable outcomes from these legal issues could damage its reputation and financial health.

Manba Finance Valuation & Recommendation

MFL has seen a significant improvement in its recent financials. However, future success depends on effectively scaling its new product lines, expanding its loan book, and maintaining asset quality. The firm’s funding costs are higher than its peers due to a lower credit rating (BBB+ by Care ratings) and a moderately high proportion of fixed-cost borrowings (66%).

The IPO is set at a price-to-earnings (P/E) ratio of 14x based on FY24 earnings. Compared to other mid-sized and larger NBFCs, which offer more diversified portfolios, the IPO's valuation appears less favourable.

Given the modest scale and regional focus of its operations, a moderately diverse product line-up with significant exposure to small, economically vulnerable borrowers, and an average funding profile, long-term investors may find better opportunities elsewhere in this sector. Nevertheless, with a 50% grey market premium and the current euphoria around recent IPOs, those willing to take on more risk might consider subscribing to the IPO for potential listing gains.

For a deep dive into other IPOs, explore: IPO Corner on Liquide

Discover Investment Opportunities with Liquide

Unlock the potential of informed investing with Liquide, featuring pioneering tools like LiMo, an AI co-pilot for stock investing. Available on both Google Play Store and Apple App Store, Liquide offers up-to-date market analysis, expert recommendations, and real-time insights to guide your investment decisions. Download today and enhance your financial journey with Liquide's cutting-edge features.