HDFC Bank Shares Plunge Over 8% Despite 39% Profit Growth: Here’s Why

HDFC Bank's shares witness a sharp fall despite significant growth: Analysing the underlying causes

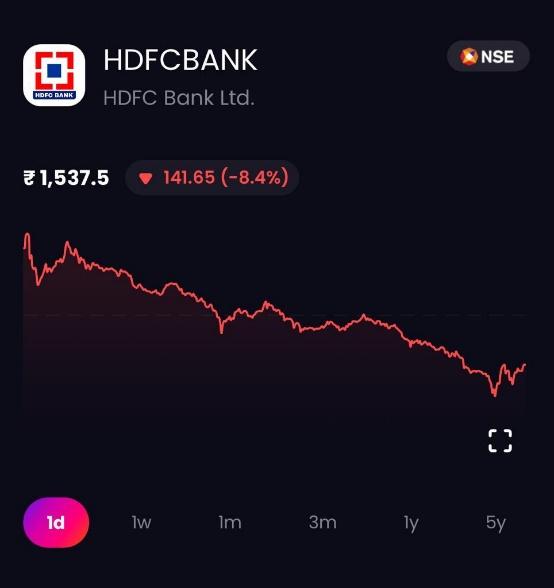

On January 17, HDFC Bank's shares witnessed a substantial fall of more than 8%, marking their steepest decline since March 2020. This downward trend followed a 7% fall in the US-listed ADRs. Despite meeting headline expectations, the bank's financial results for the October-December quarter revealed underlying issues that disappointed investors.

Q3 FY24 Overview: A Mixed Bag

India's leading private sector bank displayed a mixed financial performance in Q3 FY24. The bank achieved a 2.3% sequential rise in net profit, and a notable 39% increase compared to the previous year, totalling Rs 17,718 crore. This figure was in line with market projections, yet it included a one-off write-back of Rs 1,500 crore of tax provisions pursuant to a favourable court decision. However, the bank's Net Interest Income (NII) fell short of expectations, recording Rs 28,470 crore.

Regarding asset quality, the bank reported a decrease in gross non-performing assets (NPAs), which stood at 1.26% of gross advances, down from 1.34% in the preceding quarter. Similarly, net NPAs were stable at 0.31%, supported by healthy recoveries and accelerated write-offs.

The bank's Total Capital Adequacy Ratio (CAR) under BASEL III norms was robust at 18.4%, significantly exceeding the regulatory requirement of 11.7%.

Challenges in the Financials

HDFC Bank saw a 50% year-on-year increase in provisions to Rs 4,216 crore, which included contingent provisions of Rs 1,220 crore towards AIF investments.

Additionally, there was a noticeable dip in the bank's core net interest margin (NIM) on total assets, which decreased to 3.4% from the previous quarter's 3.65%. Prior to its merger with Housing Development Finance Corp (HDFC) in July last year, the bank consistently maintained NIMs above 4%.

The merged entity, post-merger, faced pressure on its margins, primarily due to HDFC's elevated borrowing costs and the lower yields from its loan book, affecting the financial outcomes in the subsequent two quarters.

Valuation & Investment Outlook

Going by today’s share price reaction, the street’s sentiment towards this stock is certainly bearish. This outlook, however, is short-term. HDFC Bank continues to be a primary choice for both domestic and international brokerages for their long-term portfolios. Notably, the bank has seen a nearly 23% increase in institutional investments over the past two quarters.

Currently, HDFC Bank's stock trades at a Price-to-Earnings (P/E) ratio of 23x. The bank's management is optimistic, believing that they are on the lower end of potential margin declines and anticipating a rebound to 3.7% within the next 18 to 24 months.

Acknowledging short-term challenges, we maintain a positive outlook for HDFC Bank. The benefits from its recent merger have yet to be realized. With the Net Interest Margin (NIM) appearing to stabilize at 3.4% and expected improvements in operational efficiency, the bank is geared towards a steady increase in earnings. Taking these elements into account, we view this bank as an attractive investment opportunity for long-term investors.

Unsure whether to buy, hold, or sell HDFC Bank at current levels? Ask LiMo, world’s first-ever AI copilot for stock investing that provides both a judgement and the reasoning behind it.

For an in-depth grasp of the financial markets and potential investment avenues, delve deeper with Liquide. Boasting advanced tools like LiMo and thorough market insights, Liquide equips you with the knowledge to make informed investment decisions. Download the Liquide app now from the Google Play Store or Apple Appstore and embark on a journey of informed and successful investing.