Capital Small Finance Bank: Should You Invest Your Capital In This IPO? Check Subscription Status, GMP, Investment Recommendation

Get a detailed overview of Capital SFB’s IPO, including GMP, verdict, issue details, and the company's strengths and risks.

The initial public offer (IPO) of Capital Small Finance Bank Ltd, which kicked off on Wednesday, February 07, will close for subscription tomorrow on February 09. The Small Finance Bank (SFB) is looking to raise Rs 523.07 crore through its IPO, which consists of a fresh issue of Rs 450 crore and an Offer for Sale (OFS) of Rs 73.07 crore.

Capital Small Finance Bank IPO Timeline & Details: Everything You Need To Know

- Capital SFB IPO Price: The firm has announced a price band of Rs 445 to Rs 468 per share for its IPO.

- Capital SFB IPO Subscription Dates: Subscriptions for the IPO started on Wednesday, February 07, and will conclude on Friday, February 09.

- Capital SFB IPO Size: The firm seeks to raise Rs 523.07 crore from its initial public offer.

- How to Apply for Capital SFB IPO: Prospective investors can bid in lots, with each lot consisting of 32 shares of the company. To apply for the IPO, the minimum investment is set at Rs 14,976 (calculated as 468 x 32).

- Allotment Timeline: According to the IPO schedule, the Capital SFB IPO share allotment is expected to be finalized on February 12.

- Capital SFB IPO Listing Date: The public offer is anticipated to debut on BSE and NSE on the 14th of February, 2024.

- Capital SFB GMP: According to market observers, shares of Capital SFB are trading at a grey market premium of Rs 43 (a premium of 9% over IPO price) as of today.

Capital SFB Subscription Status

As of February 07, the first day for bidding, the IPO of Capital SFB was subscribed by 50%, with bids received for 40,77,696 shares as against a total of 81,47,373 shares offered by the bank. The retail investor segment was subscribed by 67%, while the high net-worth individuals (HNI) portion was subscribed by 38% and the qualified institutional buyers (QIB) segment was subscribed by 29%.

Prior to this, on February 06, the firm secured Rs 156.92 crore through its anchor book. Some notable institutional investors that participated in the anchor round included Nippon Life India, Whiteoak Capital, Edelweiss Tokio Life Insurance, HDFC Life Insurance Company, ICICI Prudential Life Insurance Company, Kotak Mahindra Life Insurance Company and SBI General Insurance Company, among others.

About Capital SFB

Capital Small Finance Bank began its journey as a local area bank before transitioning into a Small Finance Bank in 2016. Serving the states of Punjab, Haryana, Delhi, Rajasthan, Himachal Pradesh, and the Union Territory of Chandigarh, it provides a comprehensive suite of banking services across both asset and liability categories.

The bank's asset offerings mainly encompass agricultural loans, loans for Micro, Small, and Medium Enterprises (MSMEs), trading loans, and mortgages, including housing loans and loans against property. Unlike most other SFBs, Capital SFB targets the middle-income demographic, with annual incomes ranging from Rs 4 to Rs 40 lakhs. It has established a relationship-based banking model, ensuring a predominantly secured asset portfolio.

Strengths

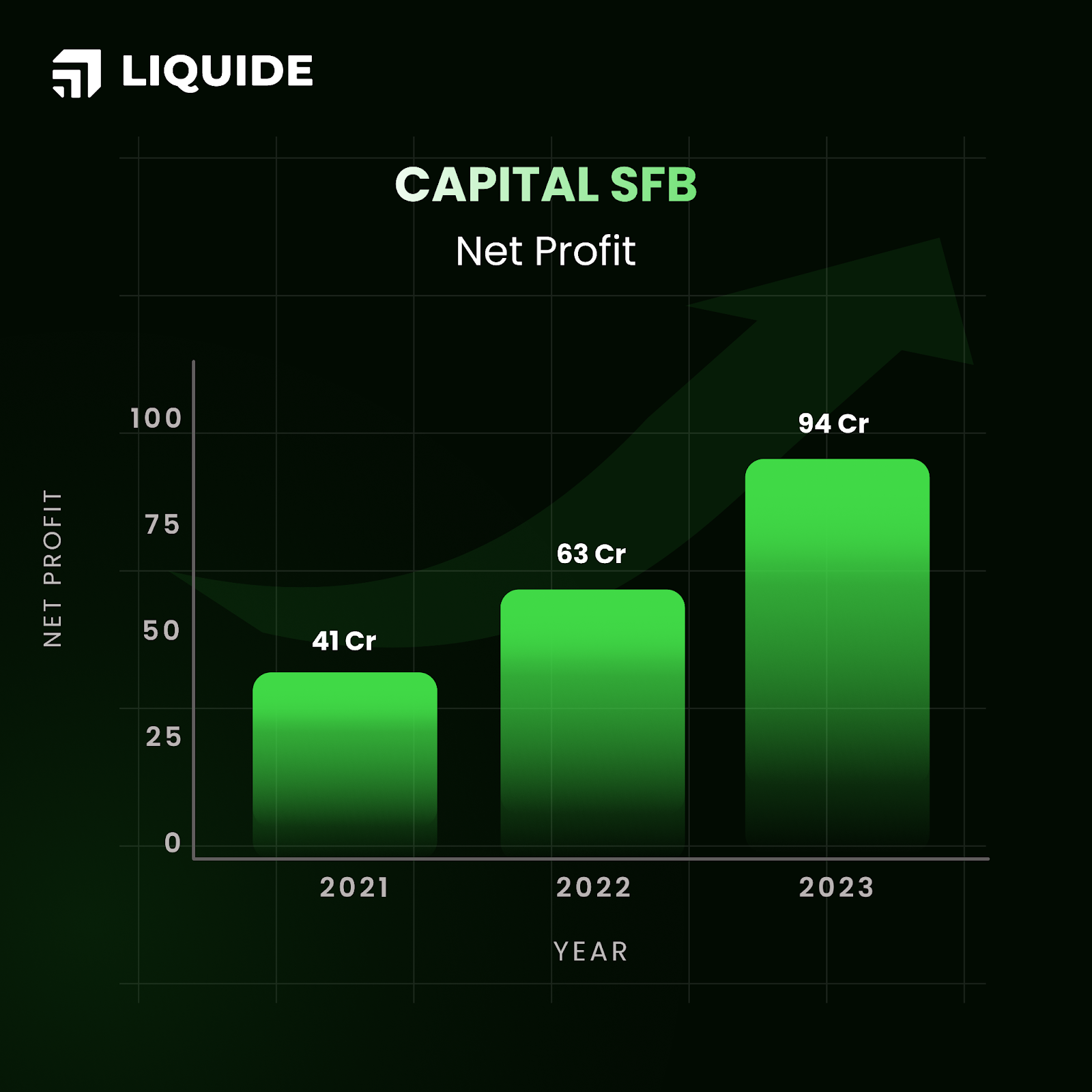

- Robust Profit Growth: Over the past three years, Capital SFB has achieved a significant compound annual growth rate of 51% in net profits, reaching Rs 93.59 crore in FY23. Furthermore, the net interest margin improved from 3.36% in FY21 to 3.74% in FY22, and then to 4.19% in FY23.

- Predominantly Secured AUM: Approximately 99.85% of its Assets under Management are secured as of H1FY24, positioning it as the leader in security among similar SFBs.

- Leading Liquidity Position: The bank maintained the highest liquidity levels on its balance sheet compared to its peers, with cash and bank balances making up 10.16% of total assets as of H1FY24. This indicates a minimal reliance on external financing for short to medium-term asset requirements and the ability to utilize surplus liquidity to expand its loan portfolio.

- Enhanced Return on Equity: The bank experienced a notable improvement in its Return on Equity, which escalated from 9.51% in the fiscal year 2021 to 16.62% by fiscal year 2023.

Key Concerns

- Geographic Concentration Risk: Capital SFB’s operations are heavily concentrated in North India, particularly in Punjab, where ~86% of its branches are located—149 out of 173 branches as of September 30, 2023. Any negative economic developments in North India could significantly impact the bank's financial performance and operational cash flows.

- Declining Asset Quality: There has been a notable decline in the bank's asset quality, evidenced by an increase in the gross Non-Performing Assets (NPA) ratio from 2.08% in FY21 to 2.77% in FY23, and a rise in the net NPA ratio from 1.13% to 1.36% during the same timeframe.

- Operational Cash Flow Challenges: The bank has faced challenges with negative cash flows from operations recently, largely due to an increase in advances, heightened investments, and the payment of direct taxes as part of normal business activities. Continuous negative cash flows could negatively impact the bank's operational performance and financial health.

- High Indebtedness: As of December 31, 2023, the bank reported a total debt of Rs 529.51 crore, comprising Rs 265.78 crore in secured loans and Rs 263.73 crore in unsecured loans. Difficulties in obtaining financing on favourable terms or managing debt obligations effectively could negatively influence the bank's business operations, creditworthiness, reputation, future prospects, and overall financial stability.

Final Verdict: Avoid

Despite some positive factors, there are a few notable concerns regarding this SFB. Capital Small Finance Bank, a modestly sized institution, has shown a 15% CAGR in advances between FY19 to FY23. This growth rate, however, is lower in comparison to larger peer SFBs. Its net interest margin is also lower than most of its peer SFBs, aligning more closely with commercial banks.

With a credit to deposit ratio of 83%, opportunities for significant credit growth are constrained in a scenario where deposits are limited. Further, with 86% of its 173 branches situated in Punjab, the bank's exposure to the economic state of a single state poses a risk.

In terms of valuation, the IPO seems fully priced with a price-to-earnings (P/E) ratio of 17x, based on FY23 earnings. This places Capital SFB at a higher valuation than most of its counterparts, except for AU SFB, which has demonstrated remarkable growth and higher return ratios in the past.

Given these considerations, investors are advised to observe the bank’s financial performance over the next two quarters before committing to any investments.

Unlock a world of financial opportunities with Liquide, the ultimate app for the modern investor. Featuring advanced tools like LiMo, India's pioneering AI co-pilot for stock investing, Liquide empowers you with insights that can guide your financial journey. Stay updated with thorough market analysis, expert recommendations, and real-time information. Download the Liquide App today from the Google Play Store or Apple Appstore and embark on a journey of informed and successful investing. Don't miss out on the powerful features that can shape your financial future.