Bharti Hexacom IPO Analysis: Should You Subscribe?

Get a detailed overview of Bharti Hexacom Ltd IPO, including GMP, verdict, issue details, subscription status, and the company's strengths and risks.

The initial public offer (IPO) of Bharti Hexacom Ltd, which kicked off today, will close for subscription on Friday, April 05. The telecom service provider seeks to raise Rs 4,275 crore through its IPO, which is entirely an Offer for Sale (OFS). The firm has announced a price band of Rs 542 to Rs 570 per share for its IPO. Prospective investors can bid in lots, with each lot consisting of 26 shares. To apply for the IPO, the minimum investment is set at Rs 14,820 (calculated as 26 x 570).

According to market observers, shares of Bharti Hexacom Ltd are currently trading in the grey market at a premium of Rs 56, i.e. a grey market premium (GMP) of 10% above its issue price of Rs 570. The public offer is anticipated to debut on BSE and NSE on the 12th of April, 2024.

Bharti Hexacom Anchor Round

Prior to issue opening, on April 02, Bharti Hexacom Ltd successfully secured Rs 1,923.75 crore by issuing 3,37,50,000 equity shares at Rs 570/share to anchor investors. This anchor round attracted participation from over 97 companies, featuring prominent funds such as Capital Group Asian Horizon Fund, Fidelity Funds, SBI Technology, ICICI Prudential, HDFC Mutual Fund, Abu Dhabi Investment Authority, Aditya Birla Sun Life, Axis Mutual Fund Trustee, Kotak Mahindra Trustee, Nipon Life, Morgan Stanley, Tata Mid Cap, White Oak Capital, and Motilal Oswal, among others.

Bharti Hexacom Subscription Status

The IPO of Bharti Hexacom Ltd received a lukewarm response on its opening day, April 3, with only 30% subscription achieved by 4pm, according to NSE figures. Marking the first major IPO of the fiscal year 2025, it attracted bids for just 1.41 crore shares out of more than 4.12 crore shares available.

The retail investor segment reached a 48% subscription rate, whereas the qualified institutional buyers (QIBs) saw a 29% uptake. Meanwhile, the non-institutional investors (NIIs) showed slightly higher interest at 36%, based on the NSE's reported data.

About Bharti Hexacom Ltd

Bharti Hexacom Ltd (BHL) operates as a subsidiary of Bharti Airtel, holding a 70% ownership stake. Specializing in communication solutions, it caters to consumer mobile, fixed-line telephone, and broadband services within the Rajasthan and North East telecommunication circles in India, encompassing states like Arunachal Pradesh, Manipur, Meghalaya, Mizoram, Nagaland, and Tripura. These services are marketed under the renowned brand 'Airtel.'

With an expansive reach, BHL boasts an extensive distribution and service network, boasting 51 retail outlets and 24 smaller format stores, spanning across 90 cities as of December 31, 2023. Furthermore, its distribution network encompasses 616 distributors and 89,454 retail touch points.

Strengths

- Dominant Market Position: BHL holds the market leader position and boasts a substantial customer base in its operational regions (Rajasthan and Northeast). The firm commands a revenue market share of approximately 40.4% in Rajasthan and 52.7% in the Northeast, with customer market shares of 35% and 49.8%, respectively, for the nine months ending December 31, 2023.

- Impressive Financial Growth: BHL has shown a strong and consistent financial growth, with a Compound Annual Growth Rate (CAGR) of 20% in operational revenue from FY21 to FY23. This period also saw a significant uptick in EBITDA by 59%.

- Rising Profit Margins: BHL has seen a steady increase in its operating profit margins, with EBITDA margin rising from 24.71% in FY21 to 43.90% in FY23, and further climbing to 49.35% by December 2023.

- Significant ARPU Growth: The Average Revenue Per User (ARPU) for mobile services has experienced considerable growth, escalating from Rs 135 in FY21 to Rs 185 in FY23, and further increasing to Rs 197 by December 2023.

Key Concerns

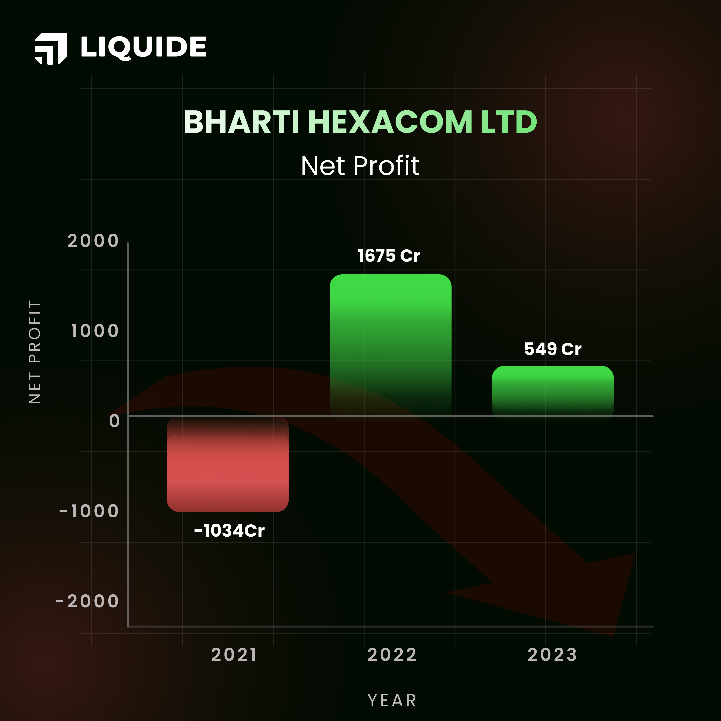

- Inconsistency in Earnings: BHL had suffered losses in FY21 when there was price war among telcos. Despite a financial turnaround in FY22 and continued growth in revenue, its profit fell again in FY23. However, management attributes this decline to a one-time accounting adjustment preceding the IPO.

- Geographical Concentration: BHL heavily relies on revenue generated from mobile telephone services in Rajasthan and the Northeast circle. Any adverse developments in these regions could potentially harm the company's operations.

- Legal Risks: BHL and its promoter are involved in ongoing legal proceedings, with amounts totalling Rs 2,405.5 crore and Rs 37,004 crore, respectively. Unfavourable outcomes in these cases could negatively impact the firm’s financial stability.

- Potential Financial Liabilities: BHL faces potential financial liabilities, with contingent liabilities recorded at Rs 275.3 crore for the nine months ending December 31, 2023. These liabilities, if realized, could negatively impact its financial health and profit margins.

- Significant Indebtedness: BHL has accumulated significant debt, with a debt-to-equity ratio of 1.4 times as of December 31, 2023. Managing this debt and adhering to lender covenants are crucial to prevent defaults and mitigate refinancing risks. Additionally, the firm requires substantial capital for capital expenditure. Failure to secure additional capital could adversely affect its business.

Final Verdict: Avoid

While BHL enjoys a dominant market position and a solid customer base, along with impressive revenue growth and increasing profit margins, there are notable concerns that warrant attention. The firm confronts challenges such as inconsistent earnings, significant legal issues, potential financial obligations, and considerable indebtedness, all of which could negatively impact its financial stability and performance post-listing.

Moreover, the IPO valuation appears to be elevated, with a Price-to-Earnings (P/E) ratio of 76x based on annualized FY24 earnings against the post-IPO fully diluted paid-up equity capital.

BHL's growth prospects seem limited as it operates only in two regions without immediate plans for expansion. Furthermore, it operates in a highly competitive industry where any resurgence of price wars could severely affect its financial performance.

Given these considerations, it might be prudent for investors to refrain from participating in the IPO, as the potential risks outweigh the rewards. Investors should wait and monitor the firm’s financial performance in the ensuing quarters before making investment commitments.

Unlock a world of financial opportunities with Liquide, the ultimate app for the modern investor. Featuring advanced tools like LiMo, India's pioneering AI co-pilot for stock investing, Liquide empowers you with insights that can guide your financial journey. Stay updated with thorough market analysis, expert recommendations, and real-time information. Download the Liquide App today from the Google Play Store or Apple Appstore and embark on a journey of informed and successful investing. Don't miss out on the powerful features that can shape your financial future.