Aastha Spintex IPO Review: Subscription Status, GMP & Analysis

Aastha Spintex IPO 2026 opens for subscription today. Read our detailed analysis of its price band, issue size, business model, financials, strengths, risks and investor outlook.

The initial public offering (IPO) of Aastha Spintex Ltd (ASL) opened for subscription today and will remain open until 1 July 2026.

As of 11:05 AM on Day 1 of bidding, the issue was subscribed 0.16 times overall. The retail portion saw 0.11 times subscription, while the non-institutional investor (NII) category received 0.29 times bids. The qualified institutional buyer (QIB) segment was yet to see participation.

Meanwhile, the grey market premium (GMP) for the IPO in the unlisted market was hovering around ₹5 per share.

Before making an investment decision, explore our comprehensive, data-driven IPO analysis to understand how the company’s numbers stack up. Our detailed report covers ASL's growth prospects, financial performance, key strengths and potential red flags.

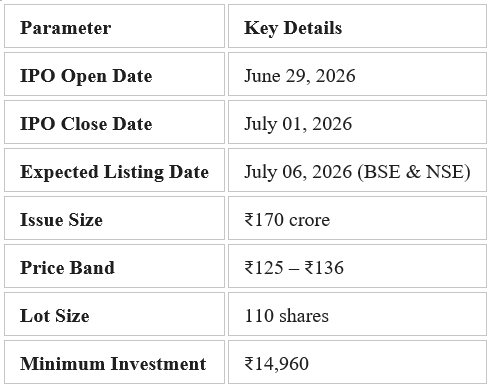

Aastha Spintex IPO Details, Date & Price Band

Aastha Spintex: Business Overview

ASL is an integrated cotton textile manufacturer with ginning and spinning operations housed within a single semi-automated facility located in Halvad, Morbi, Gujarat. The company operates across two key divisions: Ginning and Spinning, enabling it to manage cotton processing and yarn manufacturing under one setup.

ASL currently has an installed spindle capacity of 25,920 spindles supported by 15 compact ring spinning machines. Its ginning division has an annual cotton bale production capacity of 12,000 MT through 28 ginning machines, while its cotton yarn production capacity stands at 7,700 MT per annum.

Aastha Spintex: Key Strengths

- Robust Financial Growth: ASL has demonstrated strong financial performance, with revenue from operations growing at a 21% CAGR between FY23 and FY25. Profitability has scaled at a much faster pace, with EBITDA and net profit growing at CAGRs of 100% and 365%, respectively, during the same period.

- Improving Margins: ASL has witnessed steady margin expansion, with EBITDA margin improving from 4.85% in FY23 to 13.20% in FY25. Similarly, net profit margin increased significantly from 0.44% to 6.53%, reflecting better operating efficiency.

- Strong Return Metrics: ASL boasts solid return metrics, with FY25 Return on Equity of 23.21% and Return on Capital Employed of 18.89%, both higher than its listed peers. This indicates efficient capital utilisation, disciplined operations, and stronger profitability relative to shareholder equity and capital employed.

- Cost-Efficient Manufacturing: One of ASL’s key advantages is its cost-efficient manufacturing setup. Nearly 80% of its electricity requirement is met through owned solar and wind power plants, reducing dependence on expensive grid power. Since power is a major cost component in cotton spinning, lower energy expenses help the company retain better margins compared to peers.

- High Capacity Utilisation: ASL’s spinning unit operated at ~97% capacity utilisation in FY25, indicating efficient use of existing assets. This reflects strong demand visibility and better operating leverage, as the company is able to maximise output from its installed machinery.

Aastha Spintex: Risk Factors

- Client Concentration: ASL depends on a limited customer base. In 9MFY26, the top 5 and top 10 customers contributed 44.28% and 57.27% of revenue, respectively. Any loss of key customers could impact revenue, profitability and cash flows.

- Geographic Concentration: ASL’s operations are largely concentrated in Gujarat, which contributed nearly 97% of operating revenue in 9MFY26. Any adverse business, regulatory, climatic or economic development in this region could impact its revenue and operations.

- Cash Flow Concerns: CSM reported negative operating cash flows in 9MFY26 as well as FY25. If such cash flow pressure continues, it may impact liquidity, day-to-day operations and overall financial flexibility.

- Single Manufacturing Facility: ASL’s entire manufacturing operations are dependent on a single facility. Any disruption due to machinery breakdown, labour issues, raw material shortages, natural calamities or regulatory restrictions could materially impact production, cash flows and financial performance.

- Dependence on 7 Seas Impex: ASL relies significantly on 7 Seas Impex for sales outside Gujarat and exports. Under the contract, if demand from the reseller exceeds the company’s production capacity, it may need to source finished yarn from third parties, which could reduce margins.

- Raw Material Risks: Cotton prices remain highly dependent on weather conditions and global supply-demand trends. Additionally, synthetic fibres continue to compete with cotton yarn on price, while uncertainty around US tariffs on Indian textile imports could affect export demand and profitability.

Final Thoughts: Should You Subscribe to Aastha Spintex’s IPO?

ASL has delivered strong growth in both topline and bottomline over recent years, supported by healthy return ratios and improving operational efficiency.

Going forward, the acquisition of Falcon Yarns is expected to significantly expand the company’s annual yarn production capacity from 7,700 MT to 17,457 MT, giving it a much larger manufacturing base without the need to build a new facility from scratch.

ASL also benefits from its manufacturing presence in Gujarat, one of India’s key cotton-producing states, which provides easier access to raw materials.

Additionally, the company’s focus on low-cost renewable energy strengthens its cost advantage, with nearly 80% of its electricity requirement met through owned solar and wind power plants.

However, the IPO appears to be priced at a premium compared to some established peers, indicating that part of the future growth potential is already reflected in the issue price.

Therefore, investors should not expect substantial listing gains from this IPO; it is better suited as a long-term play rather than a short-term listing gain opportunity.

For a deep dive into other IPOs, explore: IPO Corner on Liquide

Disclaimer: Investment in securities market are subject to market risks. Read all the related documents carefully before investing.

The content provided in this blog is purely for informational and educational purposes only and does not constitute explicit investment advice, buy/ sell/ subscribe recommendations or a solicitation to trade.

The analysis of Aastha Spintex Ltd is based on publicly available data, the Red Herring Prospectus (RHP) and market trends. Grey Market Premium (GMP) data is highly volatile, speculative, unregulated and should not be used as the primary basis for investment decisions.

Investors are strongly advised to consult with a SEBI-registered financial advisor before executing any trading strategies or making investment decisions.

For a detailed disclaimer, please visit our official website https://liquide.life/