Weekly Review & Indian Stock Market Prediction (July 6th – 10th, 2026)

Nifty and Sensex closed higher for a fourth straight week as an IT-led rebound and cooling crude offset a rocky start driven by fresh Iran-Israel escalation. Full recap of index moves, top movers, FII/DII flows and the Nifty prediction for July 6–10.

The Indian stock market closed higher for a fourth consecutive week, navigating one of the more volatile five-session stretches of 2026 as a fresh flare-up in Iran unsettled sentiment early in the week before easing geopolitical tensions, softer crude oil prices, and strong domestic institutional buying lifted benchmarks to fresh multi-week highs by Friday.

Before the opening bell rings on Monday, let’s unpack the critical macroeconomic triggers, institutional flows and technical levels shaping the Indian stock market prediction for the coming week in this comprehensive Weekly Market Review.

Market Summary: Sensex & Nifty 50 Performance

Indian benchmark indices ended the week higher, supported by a strong rebound in IT stocks, falling crude oil prices, continued domestic institutional buying, and broad-based sectoral strength led by Realty.

The Nifty 50 gained 0.89% (214.85 points) to close at 24,270.85, while the Sensex rose 0.86% (663.44 points) to 77,763.91, extending gains for a third consecutive session.

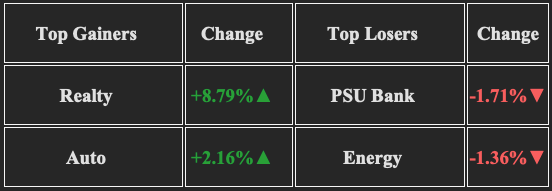

Markets remained volatile early in the week amid renewed Iran-related tensions and weakness in IT stocks. Sentiment improved from Wednesday as easing geopolitical concerns, softer crude prices, and positive global cues triggered a sharp rally, with the Nifty IT index surging 4.64% on Thursday. Meanwhile, the Nifty Realty index emerged as the week's best-performing sector, advancing 8.79% on strong buying interest across real estate stocks.

Meanwhile, India VIX declined to 11.83, a three-month low, indicating improving investor confidence. Broader markets saw selective profit booking, with midcaps underperforming while smallcaps remained largely flat.

Share Market Live News: The Big Macro Triggers This Week

1. Crude Oil Extends Its Decline : Brent crude continued its downward trajectory during the week, slipping below $71/bbl as easing geopolitical tensions and progress in diplomatic talks reduced supply concerns. The decline in oil prices is positive for India, as it helps lower the import bill, eases inflationary pressures, and provides greater policy flexibility for the RBI.

2. IT Sector Leads the Market Recovery : The IT sector emerged as the biggest driver of the week's rally after a weak start. Improving global risk sentiment, easing concerns over U.S. interest rates, and value buying sparked a sharp rebound in heavyweight stocks such as Infosys, TCS, and HCL Technologies, helping the Nifty IT index end its recent losing streak and outperform the broader market.

3. Domestic Flows Continue to Support Equities : Domestic Institutional Investors (DIIs) remained consistent buyers throughout the week, cushioning the impact of intermittent foreign selling and providing strong support during volatile sessions. Their steady inflows, combined with improving global cues and softer crude prices, continued to anchor the broader market sentiment.

Top Nifty Gainers & Losers Last Week

Sector Performance

Stock Analysis: Why They Moved

● ETERNAL: +10.89% to ₹281.65, the week's top gainer as its post-Q4 re-rating rally continued.

● MARUTI: +7.55% to ₹14,366, on a brokerage upgrade and demand optimism from easing fuel prices.

● HDFCLIFE: -4.59% to ₹567.70, the week's biggest laggard as insurance names stayed under pressure.

● LT: -4.29% to ₹4,026.60, on profit booking in capital goods after a strong recent run.

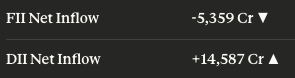

Institutional Activity: FIIs vs. DIIs

DIIs continued to aggressively absorb FII selling pressure, with Domestic Institutional Investors posting strong net inflows across all four days, while Foreign Institutional Investors remained consistent net sellers in the cash segment throughout the week.

Market Outlook & Nifty Prediction for July 6-10

Nifty enters the coming week with a constructive technical structure, having reclaimed the 24,000 psychological mark and formed a bullish crossover between its 20-day and 50-day EMAs.

Nifty 50 Trading Range: We anticipate the Nifty to trade between 24,000–24,600 in the coming week, with immediate support at 24,050 and a stronger floor at 23,900, and immediate resistance at 24,400 opening the door toward 24,600 on a sustained breakout.

Bank Nifty, which lagged the IT-led rally this past week, remains range-bound between 57,400–59,000; a decisive move above 58,500 would be needed to bring the banking pack back into leadership.

The derivatives setup shows maximum Call OI clustering around 24,300–24,500, which should act as a near-term ceiling absent a fresh positive catalyst, while heavy Put writing at the 24,100 strike reinforces that zone as a reliable support level for the week ahead.

Strategy Tip: With India VIX at a multi-month low and the Nifty testing fresh weekly highs, favour a “buy on dips” approach on quality Pharma and Financial Services names rather than chasing strength — use any pullback toward the 24,050–24,000 zone to add, and keep a tight stop below 23,900 given how quickly sentiment reversed earlier this week.

Stocks to Watch & Investment Opportunities

This week, we are tracking tactical opportunities across Pharma and Financial Services, sectors we expect to lead the tape in the coming week. You could add these stocks to your watchlist:

- Max Healthcare Institute (MAXHEALTH)

- Zydus Lifesciences (ZYDUSLIFE)

- IndusInd Bank (INDUSINDBK)

- Bharti Airtel (BHARTIARTL)

- Bajaj Finance (BAJFINANCE)

💡 Pro-Tip: Want a real-time technical analysis for these stocks? Ask LiMo, our AI co-pilot, for an instant buy/sell rating.

Discover Investment Opportunities with Liquide

Available on both Google Play Store and Apple Appstore, Liquide offers up-to-date market analysis, expert recommendations and real-time insights to guide your investment decisions.

Download the Liquide App today and enhance your financial journey.

Disclaimer: The information provided in this article is for informational and educational purposes only and does not constitute financial, investment or trading advice.

Stock, commodity and currency markets involve significant risk. Readers are strongly advised to consult with their financial advisors before making any investment decisions.

For a detailed Disclaimer, please visit our website https://liquide.life/