Weekly Review & Indian Stock Market Prediction (July 13th – 17th, 2026)

Nifty slipped 0.26% during July 6–10 as geopolitical tensions triggered a sharp mid-week sell-off despite strong Q1 updates from HDFC Bank and TCS. Read the complete weekly market recap, top gainers & losers, FII/DII activity, and Nifty outlook for July 13–17.

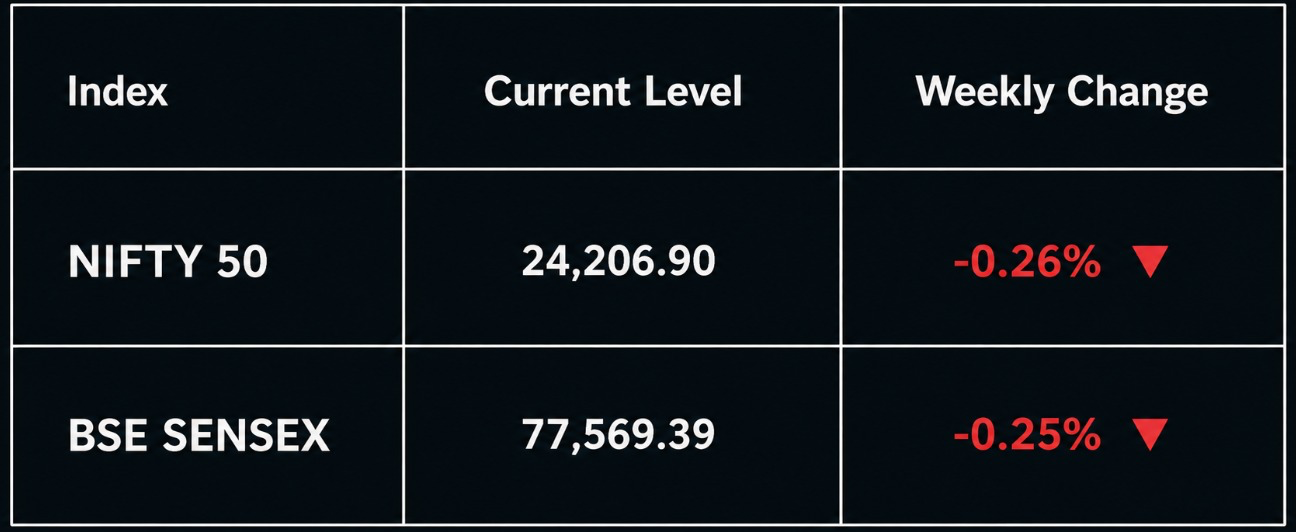

The Indian stock market ended the week of July 6–10, 2026 marginally lower, with the Nifty 50 slipping 64 points (−0.26%) to 24,207 and the BSE Sensex closing at 77,569- snapping a four-week winning streak as a violent mid-week geopolitical shock erased the gains that a stellar HDFC Bank Q1 beat had delivered on Monday. The week was one of the most dramatically bipolar in recent memory: a 200-DMA breakout on Monday followed by the worst single-session crash in over three months on Wednesday, a partial recovery on Thursday, and a TCS-powered rebound on Friday.

Before the opening bell rings on Monday, let’s unpack the critical macroeconomic triggers, institutional flows and technical levels shaping the Indian stock market prediction for the coming week in this comprehensive Weekly Market Review.

Market Summary: Sensex & Nifty 50 Performance

Indian markets witnessed a volatile week, ultimately ending with only modest losses. The rally began on Monday after HDFC Bank's strong Q1 FY27 business update boosted banking stocks, pushing the Nifty to 24,430 (+0.66%) and the Sensex to 78,285 (+0.67%), while the index closed above its 200-day moving average for the first time since February. On Tuesday, gains in IT stocks were offset by sharp profit booking in Trent and weakness in Adani stocks, leading to a flat close.

The biggest shock came on Wednesday as renewed US-Iran tensions sent Brent crude surging nearly 6%, triggering the week's sharpest sell-off. The Nifty plunged 517 points (-2.12%) to 23,882, the Sensex fell 1,677 points (-2.15%), and India VIX jumped 26% to 14.68, wiping out nearly ₹9 lakh crore in market capitalization.

Markets recovered on Thursday as bargain buying emerged, while Friday saw a strong rebound led by better-than-expected TCS earnings, PSU banks, and realty stocks. The Nifty gained 244 points (+1.02%) to close at 24,207, and the Sensex rose 828 points (+1.08%) to 77,569.

For the week, the Nifty slipped 64 points (-0.26%) from the previous Friday, while India VIX settled back near the 12–13 range after its mid-week spike, indicating that markets absorbed the geopolitical shock without a sustained breakdown. Bank Nifty underperformed the broader market, whereas Financial Services remained resilient above key support levels.

Share Market Live News: The Big Macro Triggers This Week

1. Iran Ceasefire Collapse - Week's Biggest Trigger

Renewed US-Iran tensions dominated markets after fresh strikes and retaliatory attacks ended the ceasefire. Brent crude surged above $78.8/bbl, India VIX jumped to 14.68, and nearly ₹9 lakh crore in market value was wiped out as the Nifty suffered its sharpest fall in over three months. The episode reinforced crude oil and geopolitical risks as key market drivers.

2. TCS Q1 Boosts IT Sentiment

TCS delivered better-than-expected Q1 FY27 results, with profit up 4.6% YoY, revenue up 13.9% YoY, and a ₹12 interim dividend. The stock rallied 4%, lifting the IT sector and helping markets recover strongly on Friday ahead of the broader IT earnings season.

3. Banking Updates: HDFC Bank Leads

HDFC Bank's 15.4% YoY loan growth—its strongest in five quarters—powered Monday's rally and pushed the Nifty above its 200-DMA. Axis Bank and Bajaj Finance also posted healthy business updates, while Kotak Mahindra Bank lagged on weaker deposit growth and a declining CASA ratio.

4. Crude Oil & Rupee in Focus

Brent crude jumped over 6% mid-week on geopolitical tensions, pressuring rate-sensitive sectors such as aviation, autos, and paints while weakening the rupee. As tensions eased, crude retreated toward $73–74/bbl, supporting Friday's market rebound.

Top Nifty Gainers & Losers Last Week

Top Gainers (1-Week Performance)

- SBI Life Insurance (+4.42%) – The week's top Nifty 50 gainer, supported by strong momentum in the financial services space after robust Q1 updates from HDFC Bank and Bajaj Finance. Investors rotated into defensive insurance stocks, with SBI Life outperforming during Friday's market rebound.

- Tech Mahindra (+3.92%) – Outperformed the IT sector as investors positioned ahead of TCS earnings. Better-than-expected TCS results boosted sentiment across IT stocks, helping Tech Mahindra extend its weekly gains.

Top Losers (1-Week Performance)

- Trent (-13.97%) – The biggest loser of the week after sharp profit booking erased the previous week's rally. The decline was largely driven by unwinding of crowded positions rather than any company-specific fundamental weakness.

- Dr. Reddy's Laboratories (-8.24%) – Declined as investors rotated out of defensive pharma stocks following the easing of geopolitical concerns. The fall reflected profit booking rather than any significant deterioration in business fundamentals.

Institutional Activity: FIIs vs. DIIs

Institutional flows remained firmly supportive despite heightened market volatility. Foreign Institutional Investors (FIIs) emerged as net buyers on four out of the five trading sessions during the week, with the strongest buying seen on Friday (₹2,603.72 crore) after substantial inflows on Tuesday (₹1,962.80 crore). Even during Wednesday's sharp market decline, FIIs limited their selling to just ₹532.86 crore, indicating that foreign investors largely viewed market weakness as an opportunity to accumulate rather than exit. Meanwhile, Domestic Institutional Investors (DIIs) continued to provide a strong liquidity cushion, recording net buying on four sessions, led by robust inflows of ₹3,791.42 crore on Monday and over ₹2,000 crore on both Wednesday and Friday. Overall, the combination of sustained FII interest and consistent SIP-driven DII inflows remained a key pillar supporting Indian equities despite geopolitical uncertainties and elevated volatility.

Market Outlook & Nifty Prediction for July 13–17, 2026

The Nifty enters July 13–17 at 24,207, having shaken off the worst of the Wednesday crash and regained composure by Friday’s close. The 200-DMA (now around 24,131) provided support on Thursday’s bounce, confirming the level’s dual role as resistance-turned-support after Monday’s breakout. Weekly RSI stands around 55–57 — constructive, above neutral, but not overbought. The 21-EMA has crossed above the 55-EMA (bullish crossover confirmed). Max pain for next Tuesday’s weekly expiry (July 14) sits at 24,050. The options chain shows maximum Put OI at 23,600 and maximum Call OI at 24,500, defining the likely week range.

Expected Nifty range for July 13–17: 23,700 – 24,600. Key support: 24,000–24,050 (immediate), 23,800 (strong Put OI base), 23,600 (max Put wall). Resistance: 24,400–24,500 (max Call OI cluster). A sustained daily close above 24,500 would trigger the next leg toward 24,800–25,000. Bank Nifty: support 57,000–57,400, resistance 58,400–58,500.

Stocks to Watch & Investment Opportunities

This week, we track five stocks across capital markets, housing finance, clean energy, steel and hospitality with specific near-term catalysts. Add these to your watchlist:

- CDSL - Record date July 17 for ₹12.75/share FY26 final dividend. Demat account recovery + market activity rebound support transaction volumes. Clear near-term catalyst.

- PNBHOUSING - Housing credit upcycle intact; real estate sales up 19% YoY in Q2 2026. RBI neutral stance lowers borrowing costs. Q1 FY27 results due soon. Valuation discount to peers.

- PREMIERENE - ₹3,011 crore order win (1,846 MW) announced July 7. Trading near 52W high (₹1,136). FY26 PAT +61% YoY to ₹1,510 crore. 7x capacity expansion underway.

- TATASTEEL - Safeguard duties on imports boost domestic pricing. Q1 production solid at 5.82 MT. LME aluminium rebound lifting sector; Nifty Metal up 6% MTD after June crash.

- INDHOTEL - 20 signings, 11 hotel openings in Q1 FY27. ₹3.25/share dividend approved at 125th AGM. Hospitality upcycle intact; crude easing supports inbound travel and RevPAR growth.

💡 Pro-Tip: Want a real-time technical analysis for these stocks? Ask LiMo, our AI co-pilot, for an instant buy/sell rating.

Discover Investment Opportunities with Liquide

Available on both Google Play Store and Apple Appstore, Liquide offers up-to-date market analysis, expert recommendations and real-time insights to guide your investment decisions.

Download the Liquide App today and enhance your financial journey.

Disclaimer: The information provided in this article is for informational and educational purposes only and does not constitute financial, investment or trading advice.

Stock, commodity and currency markets involve significant risk. Readers are strongly advised to consult with their financial advisors before making any investment decisions.

For a detailed Disclaimer, please visit our website https://liquide.life/