Weekly Review & Indian Stock Market Prediction (July 20th – 24th, 2026)

Nifty rose 127 points (+0.52%) in the week of July 13–17, rebounding from the previous week's decline. Tech Mahindra, TCS and Bajaj Finance led gains, while Hindalco, Trent and Grasim lagged. Strong IT earnings and Reliance's Q1 results fueled Friday's sharp rally.

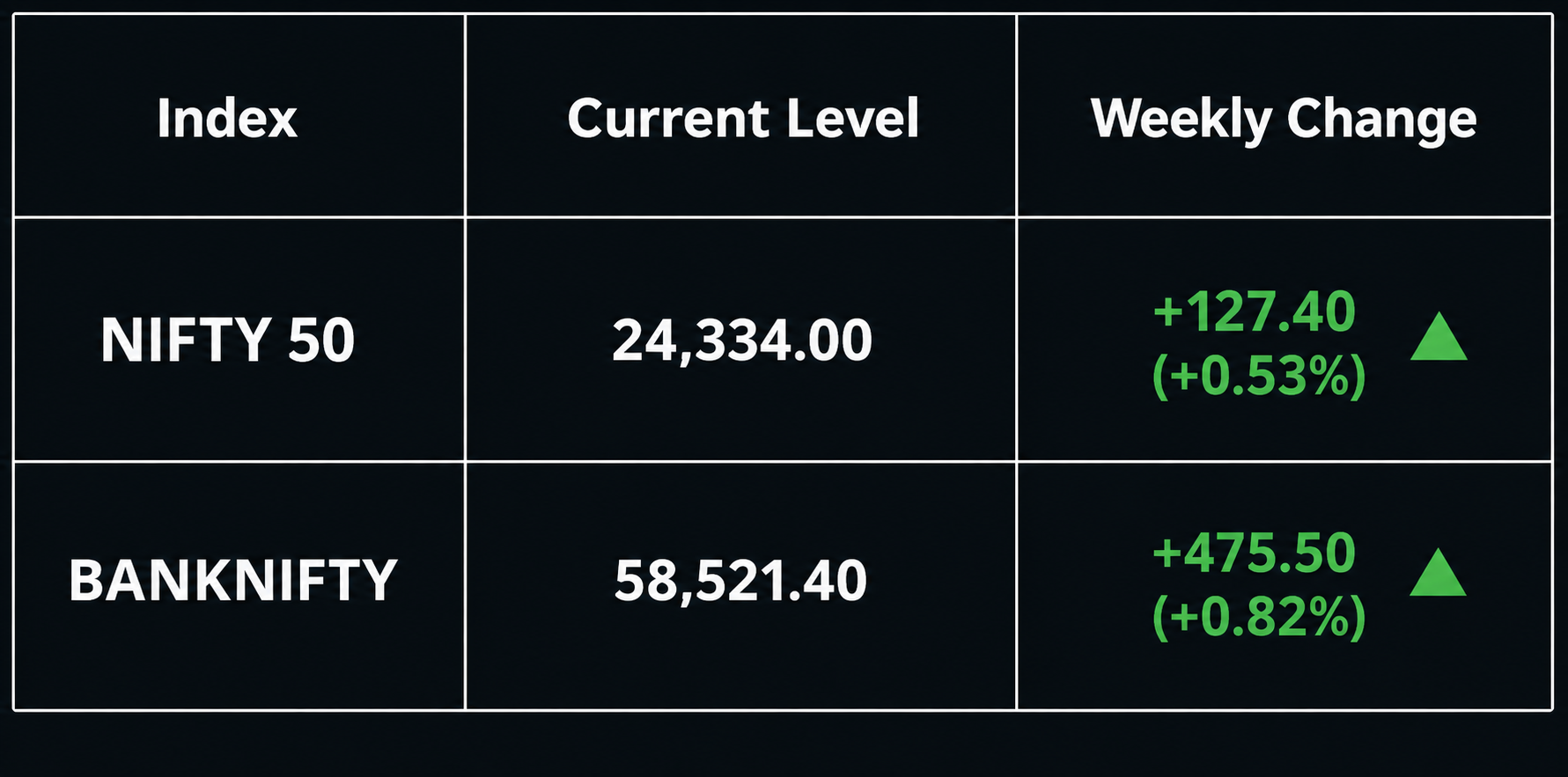

The Indian stock market returned to positive territory in the week of July 13–17, 2026, with the Nifty 50 gaining 127 points (+0.52%) to close at 24,334 and the BSE Sensex advancing to 78,151 - reversing the prior week’s Iran-triggered slip. The week delivered sharp intraday swings, a mid-week test of 23,800 support, and a powerful Friday close driven by buying in private banks, IT and auto stocks ahead of the most-watched banking results of the earnings season.

Before the opening bell rings on Monday, let’s unpack the critical macroeconomic triggers, institutional flows and technical levels shaping the Indian stock market prediction for the coming week in this comprehensive Weekly Market Review.

Market Summary: Sensex & Nifty 50 Performance

The week opened with the Nifty touching 24,530 on Monday — the week’s high — before sellers defended the 200-DMA zone for the second consecutive week, triggering profit-booking. Tuesday July 14 was the worst session: Nifty fell 159 points (−0.66%) to 24,052 and Sensex dropped 561 points (−0.72%) to 77,055, with SBI (−2.34%), L&T (−2.11%), and HDFC Bank (−1.09%) the heaviest drags. India VIX ticked up to 13.75 on the day. Auto also fell sharply — Ashok Leyland −2.71%, TVS Motor −2.15%, M&M −1.81%.

Wednesday and Thursday brought a steady recovery on easing crude oil and IT-led buying. Thursday saw Nifty Auto gain 0.61% and Nifty IT climb 1.06%, with M&M (+1.56%), Maruti (+1.42%) and HCLTech leading their respective sectors. Bank Nifty hit its weekly low of 56,549 mid-week before PSU banks staged a sharp rebound. Friday July 17 was the week’s standout: private banks surged 2.12%, the Sensex jumped 964 points (+1.25%) to 78,151, and the Nifty settled 262 points (+1.09%) higher at 24,334, driven by pre-result positioning ahead of HDFC Bank and ICICI Bank’s Saturday Q1 FY27 announcements. Week-on-week, Nifty was up 127 points (+0.52%).

Share Market Live News: The Big Macro Triggers This Week

1. Iran Re-closes Strait of Hormuz — Monday’s Gap-Down Shock

Over the weekend of July 12–13, the US and Iran exchanged fresh missile strikes, prompting Iran to declare the Strait of Hormuz closed to unauthorised vessels. Brent crude surged past $79/bbl (+4%), Nifty gapped down 167 points at Monday’s open and the Sensex fell 700+ points intraday. It was a direct replay of the July 8 crash — and confirmed that any Hormuz headline remains the market’s most powerful single swing factor. Sentiment stabilised through the week as diplomatic language softened and crude pulled back toward $75–76 by Thursday, enabling the recovery.

2. IT Q1 FY27 Earnings — TechM & Wipro Beat, Sector Re-rates

Two significant IT earnings prints changed the week’s narrative from bearish to constructive. Tech Mahindra reported Q1 FY27 net profit up 28.4% YoY to ₹1,465 crore with revenue surging 17.6% YoY — the stock’s best quarterly print in six quarters and a clear sign that its restructuring is paying off. Wipro posted revenue up 10.6% YoY to ₹24,480 crore. Together with TCS’s prior-week beat, these results confirmed that Q1 FY27 is a better-than-feared IT season, propelling the Nifty IT index to its third consecutive weekly gain.

3. Reliance Industries Q1 FY27 Results — Friday’s Big Catalyst

Reliance Industries scheduled its Q1 FY27 board meeting for Friday July 17 — the same day the Sensex surged 964 points. RIL’s Q1 results were watched for performance across its three business engines: Oil-to-Chemicals (O2C), Retail and Digital/Jio. Heavy pre-result buying in RIL shares contributed significantly to Friday’s index surge, alongside private bank positioning ahead of HDFC Bank and ICICI Bank’s Saturday July 18 announcements.

4. HDFC Bank & ICICI Bank Q1 FY27 — Weekend Results, Monday Binary

Both India’s two largest private-sector banks confirmed their full Q1 FY27 results for Saturday July 18. HDFC Bank’s Q1 NII was expected near ₹39,663 crore (+7.2% YoY) and ICICI Bank had reported Q4 FY26 PAT of ₹13,702 crore (+8.48% YoY) going into the print. Private banks surged 2.12% on Friday alone as the market pre-positioned. Monday July 20’s gap — up or down — will be the direct verdict of these Saturday numbers.

5. Fed Minutes & Global Cues — Rate Path Uncertainty Adds Headwind

The Fed’s June 16–17 meeting minutes, released this week, revealed a deeply divided committee on the year-end rate path, with AI infrastructure demand flagged as a persistent price-pressure driver. US stocks declined mid-week on AI/chip-related selling (Nasdaq −1.4%), which added to Tuesday’s Indian market caution. Asian markets were also weak — Japan’s Nikkei fell 4% on Friday, Hang Seng down 1% — providing the global macro backdrop for the week’s volatility even as domestic earnings provided the recovery fuel.

Top Nifty Gainers & Losers Last Week

Top Gainers (1-Week Performance)

- TECHM: +8.63% | ₹1,572.90 (+4.14% on Friday) The week’s biggest Nifty 50 gainer by a wide margin. Q1 FY27 PAT surged 28.4% YoY to ₹1,465 crore on revenue growth of 17.6% YoY - the company’s best quarterly print in six quarters, confirming its FY26 restructuring has turned into FY27 earnings delivery. The stock added 4.14% on Friday alone as investors re-rated the turnaround story.

- TCS: +7.78% | ₹2,269.00 (+3.09% on Friday) TCS continued to add to its post-result gains from the prior week (+4% on Jul 10). The Q1 FY27 beat — PAT +4.6% YoY, revenue +13.9% YoY, AI revenue annualised at $2.6 billion, TCV $9.5 billion - was absorbed positively across the full week as institutional buyers built fresh positions. A 3.09% Friday add-on confirmed sustained demand.

Top Losers (1-Week Performance)

- HINDALCO: −3.26% | ₹944.15 (−1.58% on Friday) The week’s biggest Nifty 50 loser. Metal stocks were caught in a double squeeze: Iran’s renewed Hormuz closure tightened global industrial supply-chain sentiment, while weaker China demand signals and a firming US dollar compressed LME aluminium prices. Hindalco’s US Novelis operations also faced margin pressure from elevated energy costs.

- TRENT: −3.12% | ₹2,842.40 (−0.62% on Friday) Trent extended its unwind for a third consecutive week (−13.97% last week, −3.12% this week) as institutional profit-booking following the prior month’s extreme rally continued. No fresh company-specific negative; the selling reflects the natural mean-reversion after excessive positioning in a high-multiple consumer discretionary name.

Institutional Activity: FIIs vs. DIIs

Institutional flows reflected a clear divergence during the week. Foreign Institutional Investors (FIIs) remained net sellers across all five trading sessions, recording total outflows of approximately ₹9,119.76 crore. The heaviest selling was witnessed on Thursday at ₹4,205.56 crore, followed by Monday at ₹3,062.27 crore, while Friday saw comparatively moderate selling of ₹376.41 crore. In contrast, Domestic Institutional Investors (DIIs) provided a strong liquidity cushion by remaining net buyers throughout the week, with cumulative inflows of around ₹9,808.64 crore. The strongest DII buying was recorded on Thursday at ₹2,986.41 crore and Tuesday at ₹2,927.71 crore. Overall, sustained domestic institutional inflows successfully absorbed foreign selling, resulting in a marginally positive combined institutional flow of approximately ₹688.88 crore and providing crucial support to Indian equities amid volatile market conditions.

Market Outlook & Nifty Prediction for July 13–17, 2026

Nifty enters July 20–24 at 24,334, above the 200-DMA (~24,131) for a second consecutive weekly close. Weekly RSI: 55.80 (constructive, above neutral). MACD: positive but narrowing histogram — a fresh catalyst is needed for the next leg.

Expected Nifty range: 24,000 – 24,800. Support: 24,200 (immediate), 24,000–24,050 (Put OI base). Resistance: 24,500 (max Call OI + 200-DMA ceiling), 24,800 (next major level). A close above 24,500 opens the path to 25,000. Bank Nifty: 57,000–57,200 support, 58,400–58,500 resistance.

Week triggers in priority order: (1) HDFC Bank + ICICI Bank Q1 FY27 results (Saturday July 18 — Monday’s gap direction); (2) Infosys Q1 FY27 results July 23 - guidance upgrade and AI TCV are the two watchpoints; (3) July 24 India-US trade deal deadline at 18% tariff — confirmed deal = immediate buy signal for IT, pharma and auto ancillaries.

Strategy Tip: Buy banking dips on Monday if HDFC Bank and ICICI Bank beat; 24,500 is the first resistance. On a miss, wait for 24,000–24,050 to stabilise. Infosys on July 23 is the IT sector’s directional pivot. Any India-US tariff confirmation is an immediate trigger for M&M, Eicher and Bajaj Auto.

Stocks to Watch & Investment Opportunities

This week, we track five stocks across Banking, finance, Auto and IT with specific near-term catalysts.

• ICICIBANK — Q1 FY27 results July 18. Q4 FY26 PAT ₹13,702 crore (+8.48% YoY). NIM at 4.40%, clean asset quality. Monday’s post-result reaction sets the week’s banking direction. Structural long.

• BAJFINANCE — +4.57% this week on AUM +24% YoY. Full results due soon. RBI neutral stance lowers borrowing costs. Best retail NBFC franchise; momentum intact.

• TECHM — +8.63% this week on Q1 PAT +28.4% YoY. Restructuring complete, earnings delivery confirmed. Infosys Jul 23 result is the IT sector’s next directional signal.

• EICHERMOT — Muted week vs. auto peers = catch-up potential. 8.4% Nifty Auto weight. Festive-season Royal Enfield demand building. India-US 18% tariff deal improves export economics. Q1 results due.

• M&M — +1.56% Thursday Jul 16. Strong SUV order book, EV pipeline intact. Direct beneficiary of India-US tariff deal on exports. Festive + rural demand upcycle supports FY27 volume guidance.

💡 Pro-Tip: Want a real-time technical analysis for these stocks? Ask LiMo, our AI co-pilot, for an instant buy/sell rating.

Discover Investment Opportunities with Liquide

Available on both Google Play Store and Apple Appstore, Liquide offers up-to-date market analysis, expert recommendations and real-time insights to guide your investment decisions.

Download the Liquide App today and enhance your financial journey.

Disclaimer: The information provided in this article is for informational and educational purposes only and does not constitute financial, investment or trading advice.

Stock, commodity and currency markets involve significant risk. Readers are strongly advised to consult with their financial advisors before making any investment decisions.

For a detailed Disclaimer, please visit our website https://liquide.life/