The TACO Theory: Why Markets Bet Against the War Drums

As the Iran-US war hits a ceasefire, we analyze the impact of crude oil on Nifty 50 earnings, RBI growth forecasts and the "TACO" principle’s market rally.

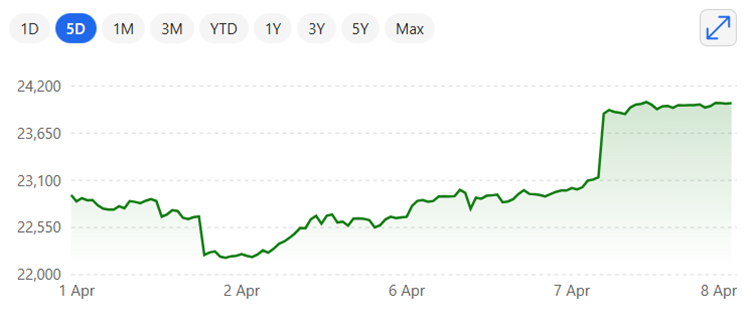

The world was staring down the barrel of a nuclear-edged West Asian conflict, but the global markets didn't blink. While headlines screamed of "obliterating civilizations," the MSCI All Country World Index (ACWI) actually rose 1.96% in the first week of April 2026.

Why? Because smart money bet on the "TACO" principle: Trump Always Chickens Out.

Behind the scenes of that high-stakes tension, the market’s intuition sensed that a retreat was inevitable. Investors saw through the "fire and fury" theatrics, recognizing them as the trademark negotiating tactics of a President who equates the health of the S&P 500 with his own political survival.

It is now obvious that the street never truly bought into the threats of "bombing Iran into the Stone Age." This skepticism was mirrored domestically; even during the peak of the hostilities, the Nifty 50 gained 3.5% in the first week of April.

Well, the bluff has been called, a two-week ceasefire is in play and oil, which had spiked on fears of Hormuz disruption, is retreating.

The 10-Point "Off-Ramp": Diplomacy or Defeat?

The 10-point proposal that Trump has labeled a "workable basis" is anything but a middle-ground agreement; it is essentially a blueprint for a total regional reset.

Far from a compromise, these demands represent a sweeping list of requirements designed to shift the balance of power in West Asia permanently.

The 10-Point Proposal Includes:

- Total Sovereignty: Iran’s absolute control over the Strait of Hormuz.

- Nuclear Legitimacy: Full acceptance of uranium enrichment.

- Sanction Erasure: Lifting of all primary and secondary sanctions, plus UN and Board of Governors resolutions.

- The Price of Peace: Financial compensation to Iran and the full withdrawal of US combat forces from the region.

If Trump treats this as a basis for a deal, he is either negotiating from a point of unprecedented vulnerability or, more likely, utilizing these extreme terms as a face-saving "off-ramp." It provides the political cover needed to exit a conflict that—true to the TACO principle—he never actually intended to finish.

The New "Controlled Corridor"

While the US-Iran truce offers a temporary breather for global shipping, don't expect a return to the old status quo. Iran is now effectively the gatekeeper, deciding who passes through the Strait of Hormuz—and on what terms.

There is a growing possibility that Iran could start slapping transit fees on commercial ships. This would essentially flip Hormuz from an open international passage into a controlled corridor.

So far, Washington has been eerily quiet about these potential "transit taxes," leaving a massive gap in how both sides are selling the deal. For the global economy, the worry is that the "cost of peace" might soon include a direct tax paid to Tehran for every barrel of oil that moves through the Strait.

India Inc: From Confidence to Crude

India entered the final stretch of the fiscal year on a high—GST 2.0 was rolling, credit expansion was healthy and trade deals with the UK, EU and US were in the pipeline.

Then, on February 28, the West Asia escalation hit. By March 4, the Strait of Hormuz was disrupted, sending Brent Crude surging 60% to cross the $120 mark and derailing the "Goldilocks" momentum.

The Fallout for the Indian Economy:

- Rupee under Fire: Smashed past the 95 per dollar mark due to aggressive FII selling.

- Slashing Growth Forecasts: The RBI has officially tempered expectations. Governor Sanjay Malhotra lowered the FY27 GDP growth projection to 6.9% (down from the previous 7%), citing the persistent drag of global headwinds.

- Stagflation Shadow: The Governor’s warning is clear: the conflict hits India through multiple "clogged" channels. Even as crude begins to retreat from its peak, it remains stubbornly high, hovering above $90.

The concern now isn't just fuel; it’s the ripple effect. Surging commodity prices have widened the current account deficit, while supply chain bottlenecks in fertilizers threaten to drag down agricultural productivity.

With global markets in flux, capital is becoming costlier just as India Inc. needs it most to navigate this high-input-cost environment.

Earnings Breakdown: Winners & the Wounded

While a "fragile ceasefire" has sparked a relief rally, the Q4FY26 balance sheets will still bear the scars of a month-long supply shock. Motilal Oswal has sounded the alarm, forecasting Nifty 50 earnings growth to plummet to just 6% YoY—the lowest in five quarters.

BofA Securities has taken an even harder line, slashing its FY27 earnings growth projection for the Nifty 50 to 8.5%, down from a pre-conflict estimate of 14%. The logic? Even with a truce, the risk of "stagflation" remains a persistent drag.

However, the market is forward-looking: if this morning's ceasefire morphs into a permanent exit from the war, expect these forecasts to be revised upward just as quickly as they were cut.

The Sectoral Scorecard

- Resilience Leaders: Financials are expected to anchor the market this quarter. Metals are also in the spotlight, as domestic steel and aluminum producers capitalize on the global commodity price surge triggered by the conflict.

- Energy Squeeze: With retail fuel prices frozen to curb inflation, Oil Marketing Companies (OMCs) have been forced to absorb the massive gap between their procurement costs and selling prices. Despite solid refining margins, retail losses and LPG under-recoveries will weigh on their bottom line.

- Margin Compression: Consumer Durables and Paints are feeling the pinch from crude-linked raw material costs. Even with oil retreating toward the $90–$95 range, the lag in price adjustments is squeezing margins thin.

- Export Volatility: Segments like Chemicals, Textiles, Engineering Goods and Auto Components are navigating a triple threat: high input costs, freight rate spikes and softened demand from Western markets. While we aren't seeing an outright earnings collapse, visibility remains clouded.

Nifty 50 Valuation

"Goldilocks has left the building," but she left behind a massive valuation gap.

As we highlighted in our previous market outlook, the Nifty 50 is trading at a forward P/E of ~17.7x. While this has edged up with the relief rally, it still represents a significant ~14% discount to its recent long-period averages.

What Should Investors Do?

With tensions easing, markets will gradually shifting their focus back to fundamentals. The most meaningful signals will likely come from management commentary during the upcoming earnings calls. If "de-escalation" is cited as a key positive for Q1 FY27 input costs, the margin of safety for patient investors has never been more attractive.

We’ve said it repeatedly—near-term volatility is the price of admission. Instead of reacting to daily swings, use this phase for structured, staggered accumulation. Building positions while the "clouds are clearing" ensures you are best positioned once the sun finally breaks through.

That said, while the ceasefire provides an important psychological boost to markets, it may still be premature to draw definitive sectoral conclusions in the near term, as geopolitical risks have not fully disappeared.

But as the immediate noise around the conflict subsides, earnings trajectory and macroeconomic trends are likely to remain the primary drivers of market direction.

Disclaimer: This news is solely for educational purposes. The securities / investments quoted here are not recommendatory. Investors are advised to consult with their financial advisors before making any investment decisions.

For detailed Disclaimer, please visit our website https://liquide.life/