ICICI Bank Q4 FY26 Results: Net Profit Beats Estimates at ₹13,702 Cr

ICICI Bank surpassed Street estimates in Q4 FY26, posting a net profit of ₹13,702 crore. With asset quality improving and a ₹12 dividend declared, find out why global brokerages remain bullish on the stock.

Stocks in News | ICICI Bank Ltd (NSE: ICICIBANK) released its Q4 FY26 and full-year financial results on April 18, 2026. The private sector lender demonstrated resilient growth, exceeding street expectations despite macroeconomic headwinds.

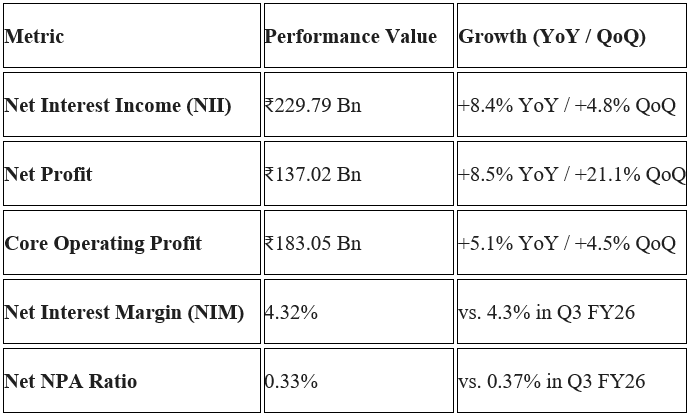

ICICI Bank Q4 Results 2026: Key Financial Highlights

ICICI Bank reported a Net Profit of ₹13,702 crore for the fourth quarter, marking an 8.5% YoY growth and a significant 21.1% sequential (QoQ) increase. This surpassed analyst estimates of ₹12,949 crore.

The bank’s bottom-line growth was primarily driven by strong growth in Advances and low credit costs, which helped offset rising employee expenses and treasury losses.

Operational Performance & Asset Quality

The bank's balance sheet remains healthy, characterized by credit growth and industry-leading asset quality:

- Loan Book Expansion: Total Advances grew 15.8% YoY and 6.0% QoQ, reaching ₹15,538.93 Bn.

- Asset Quality Improvement: Asset quality continued to trend upward, supported by lower slippages and higher recoveries.

- Provisioning: Provisions dropped significantly to ₹96.2 crore, compared to ₹2,556 crore in the previous quarter and ₹890.7 crore in Q4 FY25.

ICICI Bank Full Year FY26 Performance Highlights

- FY26 Net Interest Income: ₹880.75 Bn (+8.5% YoY).

- FY26 Net Profit: ₹501.47 Bn (+6.2% YoY).

- Dividend: The Board recommended a dividend of ₹12 per share.

Technical View: Buy, Hold or Sell ICICI Bank?

According to our Technical Research Desk, ICICIBANK is showing a strong rebound from its key support zone near ₹1,200, indicating sustained buying interest at lower levels.

That said, the stock continues to face resistance from a descending trendline in the ₹1,400–₹1,420 zone. While the recent bounce reflects improving momentum, a decisive breakout above ₹1,420 is essential to confirm a sustained uptrend.

Until such a breakout occurs, the stock is likely to consolidate within the ₹1,300–₹1,420 range, maintaining a positive bias as long as it holds above the support zone.

💡 Pro Tip: Use LiMo, our AI-driven financial assistant, to get real-time entry and exit signals for Wipro.

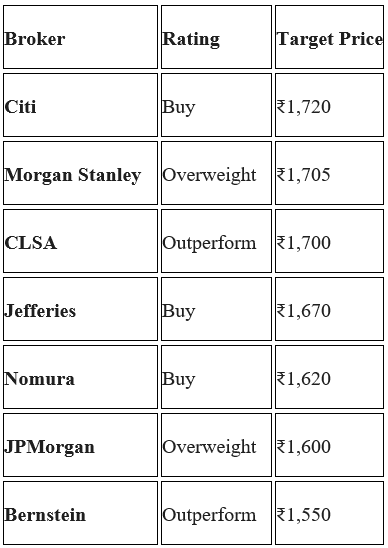

ICICI Bank Share Price Target 2026: Brokerage Ratings

Top global brokerages remain bullish on the counter:

Frequently Asked Questions (FAQs)

Q. How did ICICI Bank perform in Q4 FY26?

ICICI Bank delivered a robust performance with 8.5% YoY profit growth and a stable NIM of 4.32%. Asset quality improved with Net NPA falling to 0.33%.

Q. Should I buy ICICI Bank after Q4 results?

Most analysts maintain a " Buy" rating, with targets ranging from ₹1,550 to ₹1,700+. Use LiMo to get institutional-grade entry and exit strategies for ICICI Bank based on real-time data.

Q. Why is the ICICI Bank share price rising today?

The price is rising due to an earnings beat (₹13,702 Cr vs ₹12,949 Cr expected), a sharp drop in provisions and a dividend of ₹12 per share.

Q. What is the dividend record date for 2026?

ICICI Bank recommended a ₹12 dividend on April 18, 2026. The record and book closure dates will be announced following shareholder approval at the upcoming AGM.

Q. Is the ICICI Bank share price overvalued?

While trading at a premium to HDFC and Axis Bank, its Return on Assets (RoA) and Return on Equity (RoE) lead many analysts to categorize it as a "quality compounder" rather than an overvalued stock.

Disclaimer: This article is solely for educational purposes. The securities / investments quoted here are not recommendatory. Investors are advised to consult with their financial advisors before making any investment decisions.

For detailed Disclaimer, please visit our website https://liquide.life/