Best Ways to Invest in Gold in India: A Comprehensive Guide

From the tax benefits of Sovereign Gold Bonds (SGBs) to the liquidity of Gold ETFs and the convenience of Digital Gold, we break down the top investment options for 2026 to help you choose what fits your portfolio.

Gold has traditionally been the ultimate "safe haven" for Indian investors. Due to its inverse correlation with the equity market, the demand for gold typically surges when the Nifty 50 or BSE Sensex face volatility.

However, for many, the challenge lies in separating gold for personal use (ornamental) from gold as a strategic asset.

If you are looking to hedge against inflation or diversify your portfolio, here are the most effective ways to invest in gold today.

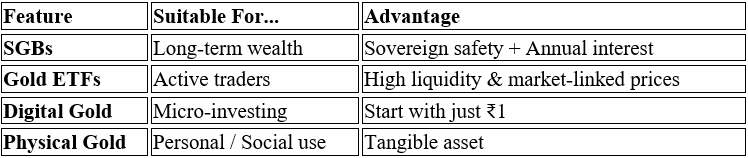

1. Physical Gold: Jewellery, Coins & Bars

Physical gold remains the most culturally significant investment in India, but it comes with distinct pros and cons.

- Jewellery: While widely popular, it is often the most expensive way to invest. Making charges (labour costs) can range from 8% to 25%, acting as a "sunk cost" that you rarely recover during a resale.

- Bullion (Coins & Bars): A more efficient physical option. These carry much lower making charges and higher purity (typically 24K).

- Risk: Physical ownership involves concerns regarding storage security, insurance and theft.

2. Digital Gold

Ideal for small-ticket investors, digital gold allows you to buy 99.9% pure gold for as little as ₹1.

- How it works: Fintech platforms partner with licensed vaults (like MMTC-PAMP) to buy and store physical gold on your behalf.

- Liquidity: You can sell it back at market-linked prices or, in some cases, request physical delivery.

3. Sovereign Gold Bonds (SGBs)

Launched by the Government of India and monitored by the RBI, SGBs are arguably the most tax-efficient way to own "paper gold."

- Returns: Aside from capital appreciation, SGBs offer a fixed annual interest (paid semi-annually); interest is taxable per slab rates

- Tenure: They come with an 8-year term and early exit option after 5 years.

- Tax Benefit: If held until maturity, Capital Gains tax is currently exempted for individuals under certain conditions.

4. Gold ETFs (Exchange Traded Funds)

Gold ETFs are units representing physical gold, traded on the stock exchange like company shares.

- Accessibility: You need a Demat account to trade them.

- Transparency: They track the domestic price of physical gold closely without the hassle of storage or purity concerns.

5. Gold Mutual Funds & FOFs (Fund of Funds)

Gold FOFs are mutual funds that invest in Gold ETFs.

- Convenience: Unlike ETFs, you do not need a Demat account; you can invest via a standard SIP (Systematic Investment Plan).

- Cost Factor: These can be slightly more expensive due to the dual expense ratio (the FOF’s management fee plus the underlying ETF’s charges).

6. Gold Savings Schemes

Many reputed jewellers offer monthly deposit schemes. You contribute a fixed amount for a set period (e.g., 11 months), and the jeweller often contributes the last instalment as a bonus.

Verdict: This is best if you have a specific event (like a wedding) planned, but evaluate the jeweller’s credibility and compare the returns against a fixed deposit (FD) before committing. If the returns from the scheme are similar to a FD or other traditional investments, the risk might not be worth it.

Key Takeaways for Investors

- The Inflation Hedge: Gold remains a premier tool to protect your purchasing power over long horizons.

- Market Volatility: During global or domestic crises, gold acts as a stabilizer for your portfolio when equities dip.

- Strategy: Limit "ornamental" gold for investment purposes. Focus on digital or paper formats to maximize your CAGR (Compound Annual Growth Rate).

Frequently Asked Questions (FAQs)

1. Is Sovereign Gold Bond (SGB) still tax-free after the 2026 Budget?

Only SGBs purchased during the primary issuance (directly from RBI) remain tax-free upon maturity. According to the 2026 tax amendments, if you buy SGBs from the secondary market (stock exchange), your capital gains at maturity are now taxable at 12.5%.

2. Which is better: Gold ETF or Digital Gold?

For long-term investors, Gold ETFs are superior because they are SEBI-regulated and more tax-efficient (12.5% LTCG after 12 months). Digital Gold is best for micro-savings (starting at ₹1), but it lacks a direct regulator and incurs a 3% GST on every purchase, which can eat into short-term returns.

3. Can I convert my Digital Gold into physical jewellery?

Yes, most platforms (like SafeGold or MMTC-PAMP) allow you to 'mint' your digital balance into coins or bars. However, you will have to pay making charges and delivery fees, which often makes it more expensive than buying a gold coin directly from a reputable bank or jeweller.

4. How much of my portfolio should be in gold right now?

Financial advisors typically recommend a 5% to 10% allocation to gold. It acts as a 'portfolio insurance' policy; while it may underperform during bull markets, it protects your capital during high inflation or geopolitical crises.

Disclaimer: This news is solely for educational purposes. The securities / investments quoted here are not recommendatory. For detailed Disclaimer, please visit our website https://liquide.life/